After weeks of blockade by Iran and the United States in the Strait of Hormuz, it is now clear that this narrow sea passage is at the center of the conflict's outcome.

The US has begun to escort ships through the narrow passage, but behind the military maneuvers lies a deeper development, the energy security in the Persian Gulf is in a state of structural realignment.

Beyond the desire of both Iran and the US to control the global flow of oil, natural gas, helium, and fertilizers from the region, the United Arab Emirates (a key US ally) withdrew from OPEC, a fact that was characterized as a significant blow to the oil cartel.

Furthermore, Iran announced plans to impose tariffs in the Strait of Hormuz as a form of reparations for the damages caused by the war.

If implemented, these fees are estimated to bring Iran between 40 and 50 billion dollars annually and will possibly allow it to mitigate, if not reverse, the impacts of American economic sanctions, but also to receive reparations for the destruction caused by American and Israeli aggression.

The crucial element is that these tariffs would constitute a means of strengthening relations with China, because they will be priced in Chinese yuan and not in US dollars.

This is expected to significantly alter regional and global power balances.

In fact, it is reported that such payments have already been made by ships destined for China, India, and Japan, while the Iranian parliament is working to officially institutionalize the process.

(It should be noted that Iran has also started accepting payments in cryptocurrencies.)

Fifty years of dollar dominance

If Iran can continue to impose these tariffs, it could shift regional influence from the US toward China and Asia, eroding the dominance of the petrodollar after the oil crises of the 1970s.

Essentially, the petrodollar system is based on the pricing and trading of oil in dollars.

The term originates from the 1970s, when the US asked Saudi Arabia to exclusively price its oil in dollars, in exchange for military aid.

This model expanded to OPEC (Organization of the Petroleum Exporting Countries), transformed into a global standard for the oil trade, strengthened the dollar as a global reserve currency, and supported American power.

The oil-producing countries accumulated massive petrodollar surpluses, too large to be invested solely in their own economies, which were channeled or "recycled" back into US bonds and stocks, as well as into sovereign wealth funds of other countries.

These funds have become the primary source of revenue for OPEC members, but also for non-OPEC oil exporters, such as Qatar and Norway.

This links these countries with Washington and gives the US significant financial influence in the global economy.

The flow of petrodollars helps finance American deficits and reduce the borrowing costs of the US.

Is a new paradigm forming?

If significant regional players such as the United Arab Emirates, Bahrain, Qatar, Kuwait, and Saudi Arabia pay the Iranian tariffs in "petroyuan", as stated by the economist Antonio Bhardwaj, this would mean "the systematic erosion of the petrodollar system and the emergence of the petroyuan as a credible, institutionally established alternative framework for the settlement of global energy transactions."

This is of course a big "if". However, the imposition of tariffs would also create a dilemma for the countries that supported Iran in the conflict (explicitly or implicitly) and for those that did not.

As the international relations analyst Pakizah Parveen wrote, we would see the emergence of "a divided global oil market: cargoes from compliant parties will transit through Hormuz in yuan, while non-compliant parties will be burdened with significantly higher costs for cargoes priced in dollars."

Such a choice would affect key US allies, such as Pakistan, South Korea, Japan, and the Philippines, all countries that have already suffered severe economic pressures due to the unrest in the Gulf and the Middle East.

Paying tariffs in petroyuan would bring them closer to China and reinforce Beijing's narrative as a reliable and more stable economic power.

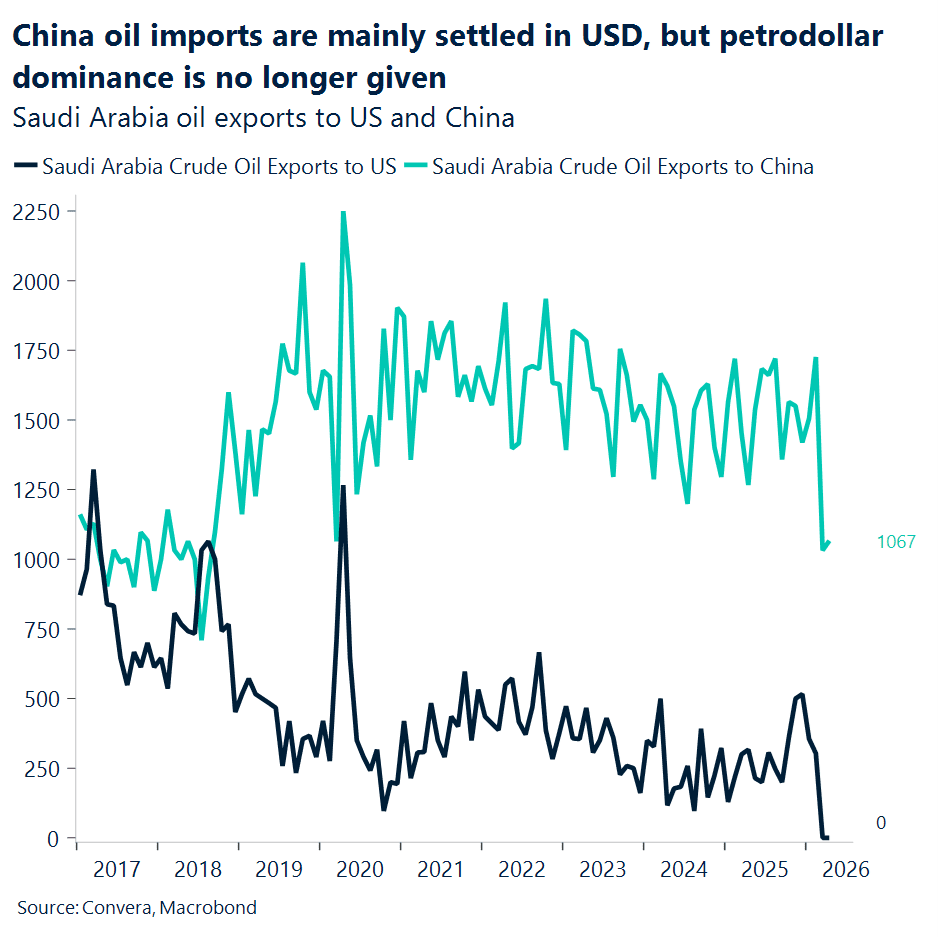

At the same time, this also reflects Russia's demand for payments for its oil in yuan since 2025.

The decline of the petrodollar

It would be premature to argue that the Iranian tariffs will lead to a generalized "de-dollarization" of the global economy.

However, they perhaps constitute a step toward the devaluation of the American dollar's significance in the global monetary system.

By extension, any distancing of other countries from the dollar also means distancing from economic and political dependence on the US.

Simultaneously, this would strengthen China's effort to internationalize the yuan.

For the first time since 1996, global central banks are holding more gold in their reserves than US treasury bonds.

The BRICS group may move even further away from American influence, as China, India, and Brazil all reduced their US holdings in 2025.

Overall, the Iranian tariffs priced in yuan would constitute yet another indication of an emerging multipolar world, in which American hegemony is no longer taken for granted.

This would mean greater strategic flexibility for all countries, large and small, but also greater uncertainty.

The difficulty of transitioning the monetary system to the yuan

A more practical question is: can someone who wants to use yuan acquire it right now?

The answer to this question proved to be much more complicated than imagined.

The largest commercial power in the world, with the most difficult currency in the market

A fact that intuitively should not exist: China is the largest commercial power in the world, but its currency is one of the most difficult major currencies in the world for someone to acquire.

In 2025, China's trade surplus reached 1.19 trillion dollars, which means that China reaps over 1 trillion dollars annually in net profits from goods traded globally.

However, in the global cross-border payment statistics, the yuan represents a mere 3%.

China earns a lot of money but spends little.

The surplus remains within Chinese borders, unexploited by the rest of the world.

If someone wants to acquire yuan, there is only one normal path: to do business with China.

Currencies and trade surpluses

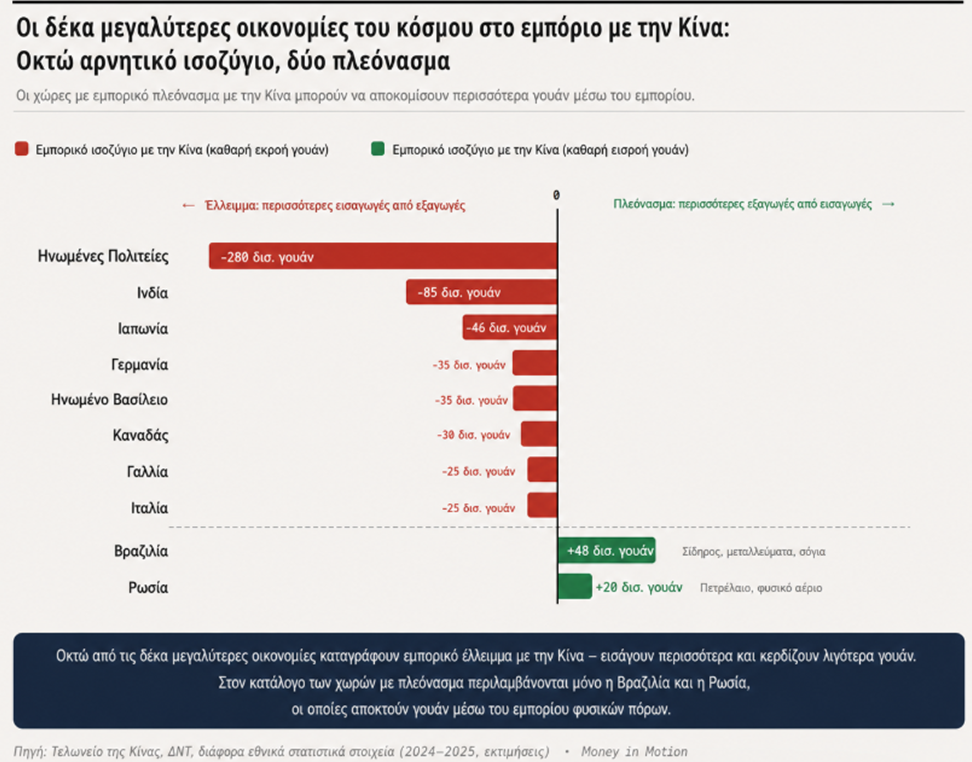

However, among the ten largest economies in the world, only Brazil and Russia have trade surpluses with China.

The remaining eight have deficits, the US has an annual deficit of 280 billion dollars, while Japan, Germany, India, the United Kingdom, France, Italy, and Canada are all net buyers, meaning a destination for Chinese exports.

The yuan leaves them, it does not enter their economies.

So, perhaps they should buy it from the financial market?

The largest offshore yuan pool in the world is located in Hong Kong, through which approximately 80% of offshore payments in the Chinese currency pass. But this pool is impressively shallow, the total global offshore RMB deposits amount to approximately 1.6 trillion yuan, while China's annual trade surplus exceeds 8 trillion yuan.

The entire pool does not correspond to even a fraction of this surplus.

Furthermore, this pool is emptying.

Three years ago, only 20% of the yuan deposited in the banks of Hong Kong was in credits.

By mid-2025, this percentage had skyrocketed over 90%, almost all the deposited money had been lent out.

Demand is increasing, but liquidity cannot keep up.

In October 2025, the Hong Kong Monetary Authority launched a liquidity provision mechanism of 100 billion Hong Kong dollars, which was immediately exhausted by 40 banks.

Three months later, the limit was urgently doubled to 200 billion, the funds were channeled through Hong Kong toward ASEAN, the Middle East, and Europe.

But these remain extraordinary measures.

The problem with foreign trade

The fundamental reason why the Chinese currency pool cannot grow is a basic structural characteristic of the Chinese economy: China is a surplus country, and the yuan returns to China through trade, instead of circulating freely in the market.

Why are there dollars everywhere?

Because the US is a country with a trade deficit, they buy goods worth hundreds of billions of dollars every year, and the dollars are "dispersed" all over the world along with this deficit.

Someone can exchange yuan for dollars on the streets of Lagos and spend dollars in the night markets of Bangkok.

With the yuan, the opposite happens, the surplus remains within the Chinese monetary space.

In March, Bloomberg cited a player in the commodities market, whose company has been settling crude oil transactions from the Middle East in US dollars for a decade. This year, for the first time, a client requested payment in yuan. He spent three weeks researching how this could be done and concluded that opening an account would take six to eight weeks, a time period that his ships could not wait.

"It is not a technical problem," he said.

"It is that you have no connection" with the yuan liquidity.

A one-trillion-dollar pool is not sufficient to cover global demand.

Gold bars from New York to Shanghai

A Greek shipowner who was asked to pay transit fees in yuan asked how he could acquire the Chinese currency and the middleman answered with one word: gold.

And this is not just a figure of speech.

Arthur Hayes, one of the most well-known macroeconomic analysts in the cryptocurrency world, described the following chain in his article in April 2026: Countries sell American government bonds → they buy gold with US dollars → they send the gold to Switzerland for recasting → they deliver it to the Chinese gold market → they convert it into yuan → and they transfer it to Iran through the Chinese cross-border payment system.

The conclusion is the following: each link of it is true individually, but the causal relationship between them constitutes a conclusion and not a proven fact.

However, each individual link is supported by market data.

Overall, they compose a fairly complete picture:

Exports of non-monetary gold from the US

In the spring of 2026, exports of non-monetary gold became the largest export category of the US for several consecutive months. Not chips, nor airplanes, nor soybeans, but gold bars.

The financial analyst Luke Gromen, examining twenty years of American trade data, said that this pattern had never appeared again.

The largest part of this gold flows toward Switzerland.

Switzerland has four of the largest gold refineries in the world, Valcambi, Argor-Heraeus, PAMP, and Metalor, which do one very simple thing: they melt gold bars from all over the world and recast them into the 1-kilogram standard preferred by China.

In 2023, China was the largest buyer of Swiss gold exports, with 25.1 billion Swiss francs.

In March 2026, Swiss gold exports to China increased by 18% on a monthly basis.

In the same month, the People's Bank of China announced that it increased its gold reserves for the 15th consecutive month, bringing its official reserves to 2,308 tons.

The main reason for the outflow of gold from the United States is in fact the reversal of the arbitrage transactions in the COMEX market in 2025, back then, due to panic from the tariffs, 43.3 million ounces of gold had flowed into the warehouses of New York and now they are starting to flow out.

This is primarily a commercial transaction.

But all these data point in the same direction: Gold flows from the West to the East and, in the most primitive form of value transfer, functions as a "translator" between two incompatible financial systems.

The assets that someone holds in the dollar world are first converted into an "intermediate form" that is recognized by both sides, gold, and then they are introduced into the yuan world.

This is how international settlements were done eighty years ago, when the Bretton Woods system was created.

Eighty years later, under the pressure of sanctions and blockades, humanity has returned to the era of the simple transfer of a metal regarding trade imbalances.

A new channel is forming2, CIPS, under the control of China

Gold is a transitional solution.

The true long-term solution is a payment system that most Chinese people are not particularly familiar with.

Let us start with what everyone knows.

SWIFT is a global "messaging system" between banks. When you transfer money from China to Japan, SWIFT informs the Japanese bank: "An amount is coming from China, this is the amount and this is the counterparty."

SWIFT itself does not move money, it only moves information.

But precisely because it moves information, whoever controls SWIFT can see the details of every cross-border transaction globally.

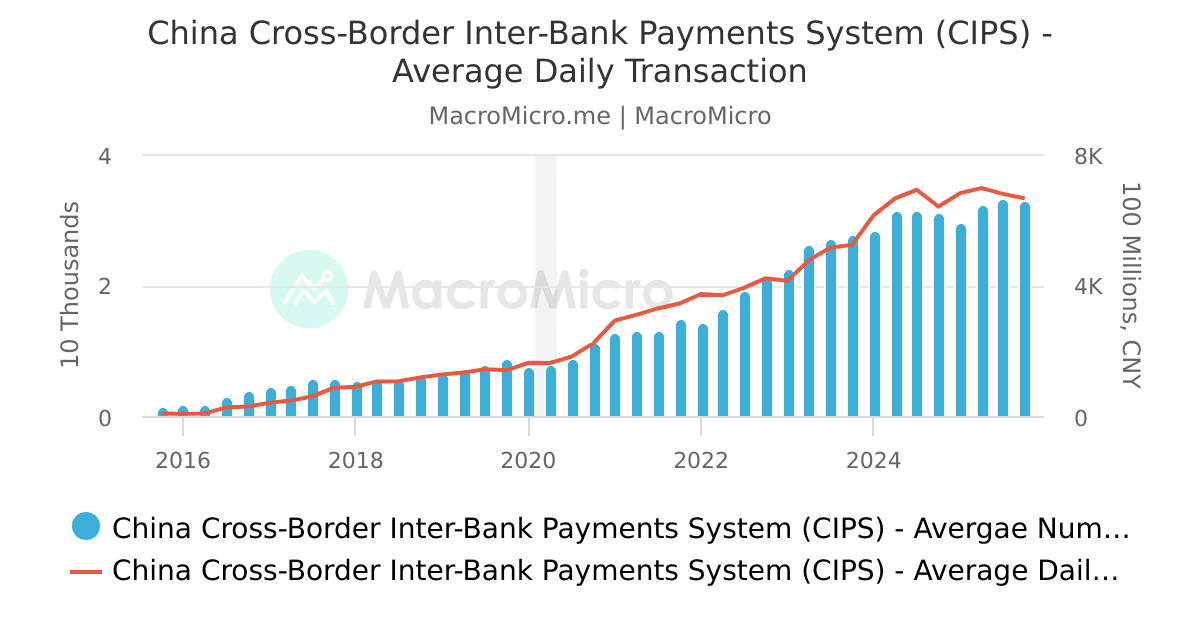

CIPS is another system that China created, a cross-border interbank payment system.

Unlike SWIFT, it can both send messages and move money, integrating message transmission, clearing, and settlement of transactions.

Most of the time, CIPS continues to use SWIFT for message transmission, about 80% of transactions work this way.

But the crucial thing is that it can also operate independently.

When needed, CIPS alone can send messages and move money.

In 2012, the People's Bank of China began the construction of CIPS.

Three years later, on October 8 2015, the system was officially launched.

On that day 19 banks were connected, but few in the world paid particular attention.

The first transaction completed was a clearing of 35 million yuan between ICBC Singapore and Shanghai Baosteel on behalf of a company.

On the same day, Standard Chartered completed via CIPS a transfer of yuan from China to Luxembourg for IKEA.

A Singaporean trading company and a Swedish furniture company.

These were the first users of CIPS.

By the end of 2025, ten years later: 193 direct participants and 1,573 indirect participants, covering 124 countries and regions and processing 26.4 trillion dollars annually.

With a rise from 19 to 193 participants, the system quietly grew tenfold.

The list of shareholders of CIPS itself is particularly interesting, the central bank owns 16%, while the remaining shareholders include UnionPay, large state banks, as well as HSBC, Standard Chartered, Citibank, DBS, BNP Paribas, and ANZ.

It is not a closed system, but a hybrid entity under Chinese leadership with the participation of Western banks.

Furthermore, the expansion is accelerating.

In early 2026, the First Abu Dhabi Bank of the United Arab Emirates joined CIPS, the first yuan clearing bank in the Gulf region, previously, settlements in the Chinese currency in the Middle East had to return to banks in China, while now they can be completed directly in Dubai.

The head of operations of DBS in China had stated to the media: "Companies have clear business reasons to use yuan, to optimize cash management, to reduce exchange costs, and to limit uncertainty."

This is not a geopolitical slogan.

They are businessmen doing calculations.

The fact that that Greek shipowner cannot buy yuan today does not mean that he will not be able to in three years. The channels are being created one by one.

What cannot be bought and what cannot return

The Greek shipowner ultimately did not manage to secure yuan. The process was too slow.

Opening an account would require weeks, the compliance checks just as many, and his ship could not wait.

Ultimately he paid in USDT, in stable coins that are pegged to the dollar.

But he did something else.

Returning to Athens, he ordered the company's financial director to investigate how they could open a yuan account in Hong Kong.

Not because it was necessary at that moment, but because he did not want to find himself again faced with an option he could not use.

He was not taking sides.

He simply realized that those who possess only one solution are excessively vulnerable in this world.

To open an additional account, to acquire an additional payment channel, does not mean that you do not trust the dollar, it means that those who have only one option are now insecure.

The gold that left the United States is now being recycled in a Swiss refinery.

It will be converted into standardized one-kilogram bars in a delivery warehouse in Shanghai, then it will be converted into yuan and channeled into some channel.

Perhaps it is for a payment of Chinese goods in the Middle East or perhaps for an ordinary payment of Australian iron ore imports from a factory in Shenzhen.

The fact that one cannot buy yuan is today's reality, what one cannot return to is the dollar channels that may be cut off tomorrow.

Those who have already found the entrance to the alternative monetary system will not turn back, it is a new monetary reality.

www.bankingnews.gr

Σχόλια αναγνωστών