The markets seem to make long cycles and today with the investment frenzy with Artificial Intelligence everything reminds of the tulip mania in Holland (1636–1637) when everything was starting for capitalism. The modern frenzy has the face of Elon Musk. SpaceX was introduced to the American market on Friday, 12 June with a valuation of approximately 1.7 trillion dollars. Elon Musk holds such a large percentage of the company's shares so that, in combination with his remaining assets, he becomes the first person in history to exceed the limit of 1 trillion dollars of personal fortune. The publicity around the event is full of the well-known exaggerations of the media: unprecedented achievement, genius, what will be his next step, what the future holds. The colpo grosso of this move that affects the financial sphere but also the point of mass deception is the exaggerated estimation of Elon Musk that SpaceX can serve the "largest exploitable Total Addressable Market - TAM in human history". His vision for potential revenues of 23.5 trillion dollars, mainly from "enterprise applications", is rather blurry and vague. Commonly he sells seaweeds... for silk ribbons. The TAMs, by definition, are characterized by megalomania.

What has happened... with technology companies

No investor is going to get excited about a startup company that targets a tiny niche market, with the possible exception of drugs for rare diseases. At the same time, TAMs say absolutely nothing about the competitive forces of the market. A mattress company, which appeals to everyone who sleeps, could claim that it possesses a potential market of over 8 billion customers. However, financial history offers also examples of today's giants that in the past underestimated their very prospects, but the danger of mass deception lurks. Let us take the positive examples. Amazon, which today possesses a stock market value of 2.5 trillion dollars, aspired to become simply the largest bookstore of the world when it was introduced to the stock market in 1997. As a substitute for the concept of TAM — a term that back then had not yet evolved into a popular business expression — they were invoking book sales in the USA, amounting to 26 billion dollars, adding indeed the corresponding global size. This might have seemed daring at that time, when Amazon was selling just one book for every one thousand distributed on a national level and was stressing that online platforms did not lend themselves to the sale of clothes and other personal items. Two decades later, however, Amazon is expected to record revenues of 824 billion dollars this year, according to the data of LSEG — more than 30 times larger than that specific estimation of the TAM. Or let us take the example of Meta Platforms, parent of Facebook. Before its founder, Mark Zuckerberg, dedicated himself to the creation of super intelligent networks, his business field was restricted to American universities — in the beginning indeed to a single university. In the prospectus of Facebook's public offering in 2012, the TAM was estimated at less than 600 billion dollars, relying on global advertising expenditures and on sales of virtual goods, such as weapons bought in electronic games. If we assume that Meta also ends up targeting the market of enterprise applications, then its today's TAM should be corresponding to the one invoked by SpaceX.

The Jevons paradox

Economic theory helps large technology companies present their revenues in a way that overturns common sense, as the chief executive officer of Microsoft, Satya Nadella, points out. He brought back to the forefront the Jevons paradox, which took its name from a Victorian economist who argued that the cheaper coal becomes, the more its demand increases — something that the supporters of artificial intelligence consider to hold true for AI as well. SpaceX has reduced by an order of magnitude the cost of transporting a kilogram of cargo into orbit and, as if by magic, satellites multiply.

Stories of investment fiction

Given these developments, Musk could perhaps let his imagination move even more freely. Why restrict the markets of the future to space tourism and to the transfer of industrial production outside Earth, when he could... cultivate the elixir of life or put an end to all wars. And why exclude Russia and China from the estimations of the TAM, when artificial intelligence might convert Homo sapiens into a single, homogeneous race that will consider Mars as the new global superpower? Besides, wherever there are people — whether it concerns tourists, expatriates, or residents of Mars — there will be a need for shops, restaurants, banks and, naturally, artificial intelligence assistants. Only the last of these categories, according to the chairman of Alibaba, Joe Tsai, could correspond to a AM of 50 trillion dollars, based on the global population of workers of the knowledge economy. This amount is double Musk's predictions for the entirety of SpaceX.

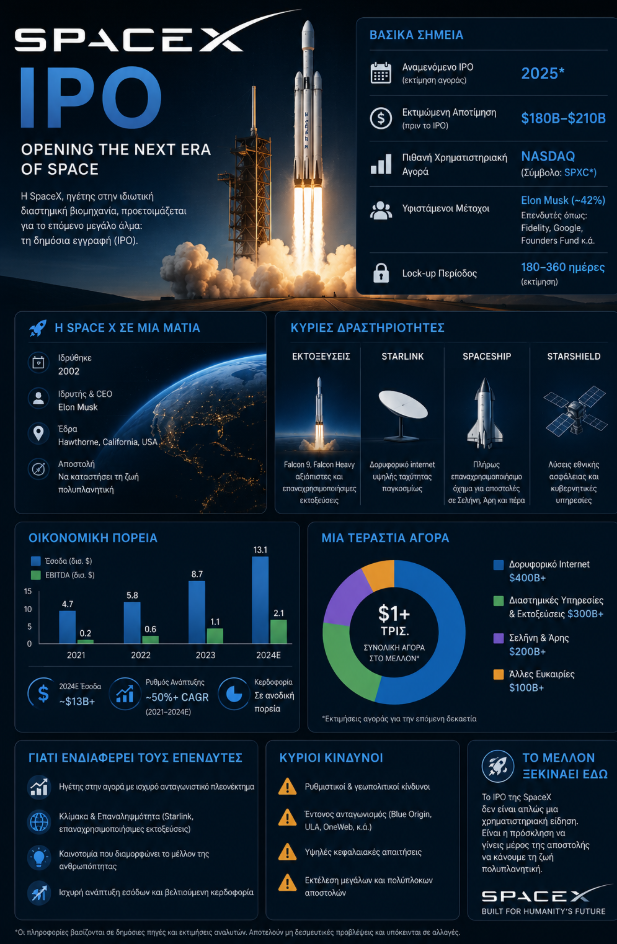

SpaceX at 1.7 trillion dollars and state subsidies

Elon Musk through this narrative seems to have invented some amazing new capability that will shape the image of humanity, but... He did not realize something that fundamentally transformed the world. He was not the first to utilize electricity. He did not invent the transistor. He did not discover rocket technology. He did not invent satellites. Nor did he even drastically improve these technologies. What he did was to learn how to utilize the system to his benefit. He took what the United States built through generations of investments and hard work and turned them into a wealth generating machine for himself. He used American loans, American intellectual property, American infrastructure, and American frequency spectrum to create a mechanism of wealth accumulation in favor of one and only man. Tesla exists thanks to a loan amounting to half a billion dollars from the American government, which was granted in 2010, when banks were not willing to finance him. The agreement provided that the Public sector would have the right to acquire three million shares of Tesla at a predetermined low price. This would be the participation of taxpayers in the success of the company, provided that it was realized. The company indeed skyrocketed developmentally. Musk, however, rushed to pay off the loan nine years earlier than its maturity, because the premature repayment canceled the right of the Public sector to the shares. The week that the repayment took place, the value of these shares amounted to approximately 270 million dollars, while since then the share of Tesla has multiplied its value many times. The Press presented the repayment as a triumph. The Public sector recovered its money with a small additional benefit from interest, while Musk maintained the shares that, according to the terms of the agreement, could have devolved to the American taxpayers. The story of SpaceX is similar, simply on a much larger scale.

How the company would not exist without NASA

In a purely capitalist system, the market system to which Elon Musk swears allegiance, SpaceX probably would not exist today. It would have collapsed in 2008. The company had exhausted its cash reserves, three rocket launches had failed, and Musk was spending the last money he possessed. Then NASA signed a contract amounting to 1.6 billion dollars for cargo transportations to the International Space Station. This money essentially financed the development of Falcon 9. Those who systematically study the space industry formulate it clearly: NASA was the one that saved SpaceX when it was on the brink of bankruptcy. And NASA, at that period, was already an organization whose resources were being gradually restricted since the decade of 1980. As a country, the United States chose no longer to develop many of the critical space activities themselves. Instead of maintaining for the Public sector the largest part of the value created through six decades of investments in rocket technology, in satellites, and in space flights, they decided to transfer a large part of this activity to private billionaires and to let them compete for state contracts. Today SpaceX maintains contracts with the American public sector valued at approximately 22 billion dollars. In the entire business empire of Musk, public funding and support approaches 38 billion dollars. The launch bases, the communications frequencies, the satellites in orbit, the first customers, and the technology that the American space program was developing over two generations constituted the foundations on which success was built. Musk utilized all these elements, while the Public sector did not maintain a substantial participation in the value produced - as it also should have. It is not argued that SpaceX does not construct efficient rockets. Its rockets work and have achieved impressive results. However, overcoming in competitiveness companies like Boeing and Lockheed Martin — two of the most traditional and cumbersome defense contractors of the USA — does not constitute an insurmountable achievement. And he achieved it utilizing technologies developed by the American space program and through contracts financed by taxpayers. At the same time, China proves today that nothing of this was the result of a single human miracle. The country still lags behind in reusable rocket technologies and in the number of launches. However, it reduces the difference quickly through a national plan that combines state enterprises, startups with state support, and satellite constellations of tens of thousands of units. Access to space is something that only a state - and indeed with the size of the USA - can decide to develop and possess. The United States, on the contrary, chose to cede this advantage to a private individual. The United States have already transferred a significant part of their productive base to China. Now, they are gradually transferring functions of the state itself to a small group of exceptionally powerful private individuals, who subsequently reassign these activities back to society on private terms. The answer, according to this logic, is not the imposition of a wealth tax. Even if higher taxes are imposed on persons like Elon Musk, Jeff Bezos, and Mark Zuckerberg, the revenues will end up in the state without the structure of the system changing substantially. If wealth is removed from Musk and channeled into a health system that already absorbs enormous economic resources before these reach the patient, the result will not necessarily be better healthcare or a larger life expectancy. Instead, the value of the health companies themselves may simply increase. Solutions are not easy like slogan-mongering.

The Ponzi scheme and the... mandatory investment

Imagine a journey... with the hypersonic train Hyperloop, which was moving inside a tunnel that The Boring Company had constructed. Using the neural implant to call a fully autonomous robotaxi of Tesla. En route you read the latest news from the Mars colony. Of course, nothing of this happened in reality, because none of these products exists. No Hyperloop operates. The Boring Company has not constructed any commercially exploitable network of tunnels. Tesla possesses few taxis with autonomous driving capabilities — not however fully autonomous — in Austin and nowhere else. (On the contrary, the autonomous taxis of Waymo, subsidiary of Google, operate already in several large metropolitan areas.) Neuralink, which aspires to pioneer in brain implants, has tested its technologies on very few patients and nothing more. And of course there is no colony on Mars: not a single manned mission to the Red Planet has been realized, nor does something like that appear in the visible future. And yet, during the duration of the last decade, Elon Musk had promised repeatedly that all these services would be available by 2025, if not earlier. Certainly, Musk has to display certain real successes. Tesla preceded in the development curve of electric vehicles, while Starlink constitutes both a critical communications infrastructure and a viable business activity. However, these achievements do not suffice by themselves to explain how Musk became the richest person in the world. His fortune was supported mainly on a self-fueling mechanism of faith: investors, convinced of his genius, were accumulating shares of companies controlled by himself, while the rise of their stock market value further reinforced his reputation as a visionary businessman. There is indeed a term for enterprises that look successful because they constantly attract new investors and constantly attract new investors because they look successful. They are called "Ponzi pyramids".

And Elon Musk is, essentially, the embodiment of the Ponzi pyramid. The public offering of SpaceX, which is in progress today, makes clearer than ever that Musk's greatest talent is not the development of technologies of the future. It is his capability to handle complex financial constructs and to utilize his influence in centers of power, particularly in the ranks of the Trump government. To make the argument understood, it suffices to remember the acquisition of Twitter in 2022, which he renamed to X. For the financing of the acquisition, investment banks granted to Musk loans amounting to 13 billion dollars, with the intention to resell the debt quickly to investors.

However, Musk deconstructed the business model of the platform, converting it — according to his critics — into a space of extreme political speech, with the result that advertisers departed en masse. By the summer of 2024, the value of X had fallen to less than half of its acquisition price. If banks attempted then to sell the relevant debt, they would record losses of the order of 40 cents per dollar. They were forced therefore to hold it much longer than they had calculated, a fact that led the Wall Street Journal to characterize the acquisition of Twitter by Musk as "the worst acquisition for banks since the financial crisis".

The rescue after the acquisition of platform X

Subsequently, however, two developments happened that rescued both the banks and the future creditworthiness of Musk: the election of Donald Trump in 2024 and the explosive rise of artificial intelligence. After the return of Trump to the White House, several advertisers returned to platform X, invoking the need to maintain good relationships both with Musk and with the new government. At the same time, in March of 2025, Musk merged the newly established artificial intelligence company xAI with X, utilizing the enthusiasm that was prevailing around AI to support both the valuation of the platform and his own financial position. The problem is that Grok, the artificial intelligence model of xAI, is considered by many analysts noticeably inferior to the corresponding systems of Anthropic and OpenAI. At the same time, it has received intense criticism for issues of reliability and safety. In a characteristic case, it produced racist and antisemitic content, reaching the point of calling itself "MechaHitler". Despite the efforts of officials of the Trump government to promote the use of Grok in federal agencies, including the Pentagon, the results have been limited. Thus, according to the author, Musk initially rescued X integrating it into xAI and now attempts to rescue xAI integrating it into SpaceX — a company that possesses indeed a successful and profitable business model through Starlink. Today SpaceX is introduced to the stock market and its public offering on Nasdaq takes place with a valuation that approaches 1.77 trillion dollars, although its revenues amounted last year merely to 18.7 billion dollars and the company remained loss-making.

How can such a, literally, astronomic valuation be justified?

The public offering relies partly on the hypothesis that private investors will buy shares not because they rationally evaluated SpaceX as an enterprise, but because they believe that they acquire participation in the "genius" of Elon Musk. However, his faithful followers may not suffice to sustain indefinitely this financial edifice. For this, Musk's allies on Wall Street attempt to alter the rules of the game. Certain important stock market indexes, such as the Nasdaq 100 and FTSE Russell, modified recently their regulations so as to allow the almost immediate inclusion of SpaceX. The significance of such a move is enormous. A large part of global investments is directed through passive investment funds (index funds), which are obliged to buy shares of companies included in the basic indexes. With other words, inclusion in an important index automatically creates new demand for the share of a company. Traditionally, the large indexes were waiting at least one year after the introduction of a company to the stock market before examining its inclusion, so that the share acquires a sufficient trading history and "matures". The fact that the rules changed for SpaceX constitutes yet another indication of Musk's capability to influence and adapt critical institutions to his benefit. An exception constitutes the S&P 500 index, which refused to yield to the pressures and maintained its minimum waiting period of one year.

The Ponzi pyramid

The enormous "human Ponzi pyramid" that Elon Musk represents will collapse at some point. There is however a critical difference from traditional Ponzi pyramids. Usually, only those who voluntarily chose to participate are harmed. This time, a large part of the capital supporting the edifice of Musk originates from millions of Americans who, essentially, do not have a choice. Approximately 52% of the assets of mutual funds in the USA is placed in index funds, while over half of American households possesses a participation in such types of investment products. The collusion between Musk and Wall Street, in combination with the perception that the Trump government supports the billionaire businessman, leads millions of small investors to participate, willingly or not, in the financing of his constantly expanding empire.

The fraud in the idea of data centers in space

Elon may possess enough money to secure a seat on every space launch, but it seems he omitted certain basic lessons of physics in high school. Space is not "cold" in the way a freezer is cold. Space is an empty, inhospitable vacuum. And the vacuum does not allow heat to escape easily. Let us remember therefore how heat is really transferred. There are three basic mechanisms:

1) Conduction, like when we touch a hot stovetop.

2) Transfer or convection, like when a cool breeze cools sweated skin.

3) Radiation, where heat is transmitted through electromagnetic waves.

On Earth, data centers are maintained at safe temperatures thanks to enormous air conditioning systems. It concerns a process of convection: heat is transferred from electronic circuits to the air and subsequently the air is removed mechanically. This system works efficiently. In the vacuum of space, however, there is no air. There is no water. Therefore, both convection and conduction become essentially impossible as methods of cooling. The only available mechanism of heat rejection is radiation, which is considered the slowest and least efficient way of thermal discharge in comparison to the other two. If a data center is installed in space, its electronic systems will produce enormous quantities of heat which it will be exceptionally difficult to reject. To achieve sufficient cooling exclusively through radiation, giant surfaces of thermal cooling mechanisms (radiators) would be required, possibly of a size corresponding to football fields, so that they offer enough surface for the emission of heat into space. This creates an additional problem: such constructions would be bulky, heavy, and exceptionally expensive in their transportation and installation in orbit. And the situation becomes even more complex if the Sun is taken into account. The enormous nuclear fusion reactor at the center of the solar system constantly emits enormous quantities of energy in the form of solar radiation. Every time a space data center is exposed directly to sunlight, it receives a strong thermal load from an external source. With other words, the problem is not only the rejection of the heat produced by the computers themselves. It is also the need of managing the additional heat absorbed from the environment. The idea that the transfer of computing infrastructure to space constitutes a self-evident solution for the energy needs of artificial intelligence relies more on science fiction patterns rather than practical engineering. Elon Musk simply reproduces incomplete science fiction ideas that he read at a young age, repackages them with the language of the modern technology industry and hopes that the public will not notice a fundamental reality: The laws of thermodynamics do not care about the capitalization of a company nor about the price of its share. Despite all this, Media like Axios sell the fairytale in order for more money of Americans to flow for the controversial venture: "... Other factors make exceptionally difficult the construction and operation of data centers outside the atmosphere of Earth, including the cost of launching the equipment and the challenge of maintaining and upgrading systems. Even cooling is much more difficult in space than many assume. Because in space there is no air, electronic systems that develop heat cannot reject it through transfer of heat with currents (convection), as happens on Earth. Contrary, data centers in orbit need large cooling mechanisms with radiation (radiators) to remove heat through radiation" ...

Let us see how long the joke will last... But probably it will not end with laughs, but with cries for the lost savings, while Musk will be counting the trillions of dollars.

www.bankingnews.gr

Σχόλια αναγνωστών