The President of the US, Donald Trump, finds himself faced with one of the most difficult decisions of his second presidency, a situation in which he found himself based on his own decisions, as he started the unnecessary war with Iran with the nod of genocidal Israel.

As he considers whether to pursue a new escalation against Iran or move toward a de-escalation agreement, the tools that until today held back international oil prices are depleting at a rapid pace.

This is the warning of the former White House special advisor on energy issues, Amos Hochstein, who argues that the two largest geopolitical crises of the era, Russia and Iran, are beginning to function as a unified energy front, while the margins for Washington to absorb a new shock in the markets are nearly disappearing.

As he noted in a series of posts on the platform X: "As Trump weighs escalation or a deal, he faces a harsh reality: the Russia and Iran fronts are merging and the tools for managing the next energy shock are disappearing week by week."

As Trump weighs escalation or a deal, he's confronting a harsh reality — the Russia and Iran fronts are coalescing, and the tools to manage the next energy shock are disappearing week by week.

— amos hochstein (@amoshochstein) July 16, 2026

?

1/ When the Hormuz MOU was announced, transit relief flowed to crude — not diesel,… https://t.co/Lb87ME7jsA

Attention: The real crisis is in fuels

Although following the partial restoration of navigation in the Strait of Hormuz crude oil exports have increased, this image is misleading.

According to the International Energy Agency, IEA, global oil production increased by approximately 4.1 million barrels per day in June. However, it still remains approximately 9.4 million barrels per day lower than the levels before the start of the conflict.

The most important problem now is not crude oil but the production of refined products.

Exports of diesel, gasoline, jet fuel, and liquefied petroleum gas from the Persian Gulf countries remain below 50% of pre-war levels, while most Middle East refineries continue to operate at limited capacity.

Concurrently, Ukrainian strikes on Russian refineries have significantly reduced Russian fuel production, while several Asian units also continue to underperform.

The result is a paradoxical image: crude oil prices have not skyrocketed, but diesel and gasoline prices remain at particularly high levels.

As Hochstein emphasizes: "The biggest problem now is not whether crude oil exists, but whether the capability exists to convert it into fuels."

Attacks on Russian refineries restrict supply

According to the former White House advisor, the Ukrainian attacks on Russian energy installations forced Moscow to impose a total ban on diesel exports.

Russia covers approximately 11% of the global diesel market and this decision had immediate consequences.

Russian exports of diesel and other energy goods were restricted at the beginning of July to approximately 234,000 barrels per day, against an average of 817,000 barrels in 2025.

This development caused a rise of approximately 11% in diesel contracts in the United States, while the premium of European gas oil against Brent reached historic highs.

Diesel constitutes a basic fuel for transport, agriculture, construction, and electricity generation.

Therefore, every new shortage translates into higher costs across the entire economy.

The US has nearly exhausted its margins of reaction

The most important warning of Hochstein concerns the American market itself.

Refineries in the US are already operating at 96.2% of their capacity, processing approximately 17.1 million barrels per day.

With such high utilization, there is little margin for a further increase in fuel production.

At the same time:

1) gasoline stocks are approximately 8% below the average of the last five years,

2) diesel and heating oil stocks are approximately 11% lower,

3) while commercial crude oil stocks fall short by approximately 6% of normal levels.

Reserves at a critical point

The situation in Cushing, Oklahoma, the most important oil storage center in the United States, also causes concern.

Reserves have fallen below 20 million barrels, approaching the level that the industry characterizes as tank bottoms, meaning the minimum limit below which even the operation of tanks and pipelines becomes difficult.

The Strategic Petroleum Reserve no longer constitutes a safety net

Equally worrying is the situation of the Strategic Petroleum Reserve, SPR.

American strategic reserves now amount to approximately 316.5 million barrels, meaning more than 86 million barrels less compared to a year ago.

Hochstein连warns that they will soon fall below 300 million barrels, dramatically restricting the capability of Washington to face a prolonged energy crisis.

Even a new release of reserves, however, would not solve the basic problem, as American refineries are already operating nearly at the maximum of their capabilities.

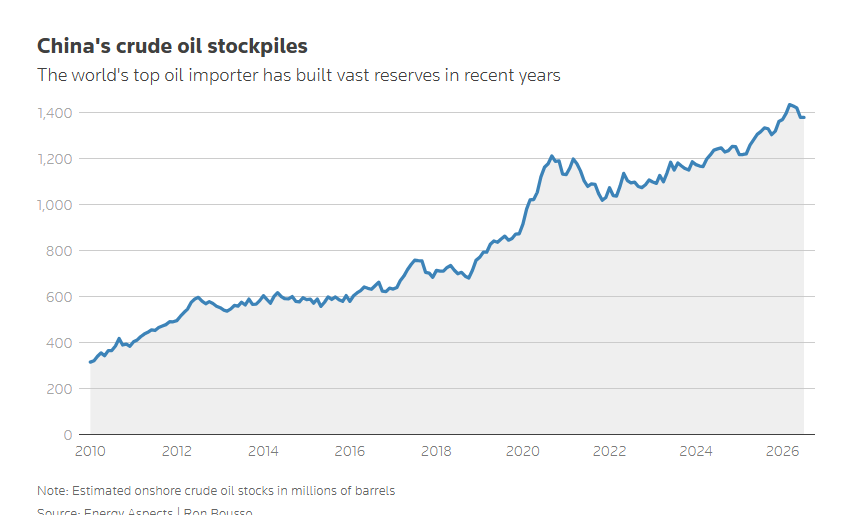

China will not continue to hold back prices

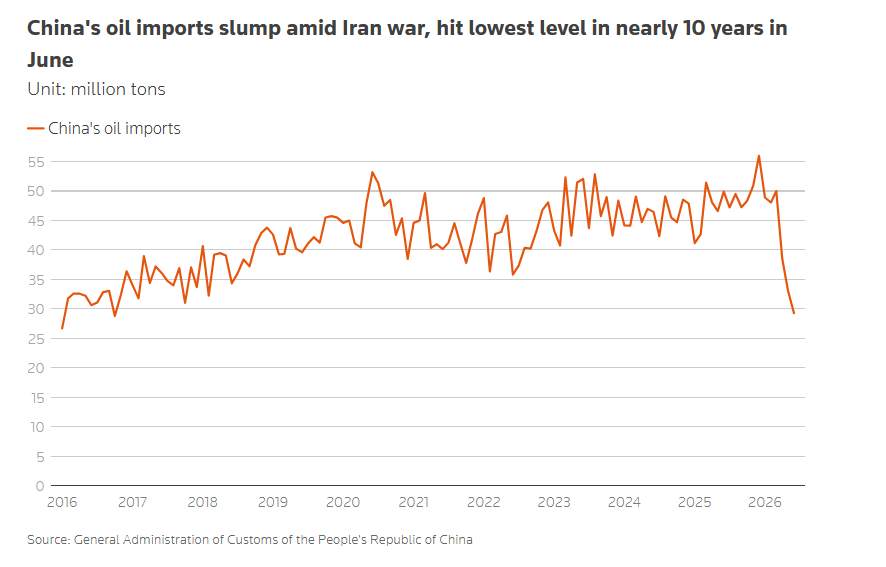

One of the basic reasons that oil prices did not skyrocket after the crisis in the Strait of Hormuz was the stance of China.

Between February and May, Beijing restricted oil imports by approximately 4.5 million barrels per day, utilizing the massive strategic reserves it had created before the start of the crisis.

In June, Chinese imports fell to the lowest level of the last decade, approximately 7.12 million barrels per day, meaning by more than 41% compared to a year ago.

Analysts estimate that China utilized hundreds of millions of barrels from its reserves, which are calculated between 1.2 and 1.3 billion barrels.

However, this "shield" seems to be depleting.

According to Goldman Sachs and the IEA, Beijing has already begun using its reserves and may soon return dynamically to international markets to replenish them.

This means that the most important factor restricting international oil demand in recent months might cease to exist.

Amrita Sen, head of the consultancy firm Energy Aspects, estimates that since the start of the crisis the global market has consumed approximately 600 to 700 million barrels of available reserves.

Speaking to the Financial Times, she warned: "Now there is almost nothing left of the surplus reserves."

In her interview with CNBC, she was even more pessimistic: "If the situation remains the same until the end of this month or the beginning of the next, we have not seen the worst yet.

The most difficult will probably come later, in the third or at the beginning of the fourth quarter."

Time exerts suffocating pressure on Trump

All this composes an extremely difficult equation for Donald Trump.

If tension with Iran reignites and navigation in the Strait of Hormuz is interrupted anew, the global market no longer possesses the reserves, the surplus production capacity, and the reduced Chinese demand that until today absorbed the shocks.

With American strategic reserves decreasing, refineries already operating nearly at maximum, Russian fuels missing from the market, and China preparing to return as a large buyer, the margins of reaction for Washington are narrowing dangerously.

The conclusion of Amos Hochstein is clear: the "defenses" that protected the energy market are depleting.

If there is no de-escalation soon, the world from September may find itself faced with a new energy crisis, with significant consequences for inflation, economic growth, and the cost of living internationally.

www.bankingnews.gr

Readers’ Comments