The picture in the markets of Japan is beginning to resemble a slow but persistent phase shift in a system that for decades operated with artificial stability.

From savior of the monetary system, during the Nixon shock with the largest monetary agreement in history, it is now expected to become the destroyer of a leveraged financial system.

Just as Greece represented the sins of a monetary system — the Eurozone — with states moving at different fiscal speeds, so too will Japan burst, emphatically highlighting the end of the era of zero interest rates and cheap money.

The yen is moving around 162 units against the dollar, levels that point to 1986, while the market is now no longer simply discussing further weakening, but whether the next big range lies at 170 or even 200 yen/dollar.

At the same time, the bond market shows a parallel crack.

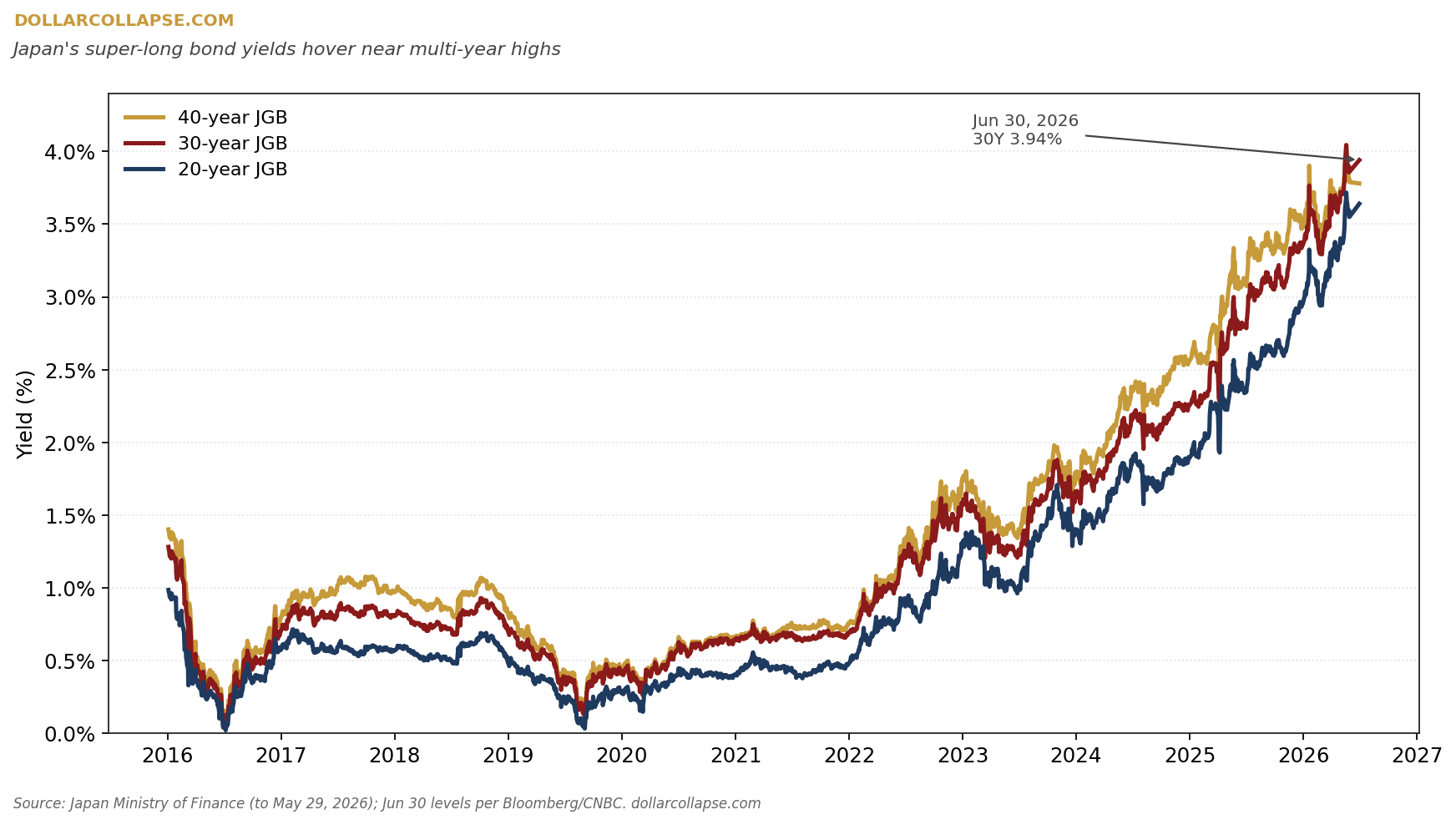

The yields of long-term Japanese government titles are rising steadily, with the 30-year bond approaching 4%, in an economy where public debt fluctuates between 240% and 260% of GDP.

For decades, this combination was considered almost impossible: a state with such high debt and such low financing costs. Now, however, this balance is beginning to shift.

The story behind this transition essentially begins from 1985 and the Plaza accord in 1985, when the sharp appreciation of the yen pressured the Japanese export model.

The response of the Bank of Japan was an aggressive easing that, instead of stabilizing the economy, contributed to the creation of the big bubble at the end of the 1980s.

When this collapsed in the early 1990s, Japan never returned to a "normal" monetary policy regime.

Successive waves of intervention followed.

The zero interest rates at the end of the 1990s, the first QE in 2001, and then the big turn of 2013 with Haruhiko Kuroda and the QQE policy, where the central bank initiated massive purchases of government bonds and ETFs, gradually transforming into the dominant player of the very market it is supposed to regulate.

The result of this long path is that today the Bank of Japan does not operate simply as a central bank, but as a key financier of the Japanese state.

Its balance sheet has reached levels comparable to the country's GDP, while its presence in the bond and stock markets remains decisive.

The subversion of the balance

However, this balance is beginning to be tested from two directions simultaneously.

On one side, the currency is weakening in a persistent and almost absolute way.

Despite interventions of the order of 11.7 trillion yen, or approximately 72.8 billion dollars, the yen continues to decline.

On the other, the yield curve itself is beginning to proceed with a repricing of risk, as the BOJ is forced to move from absolute interest rate suppression toward a very gradual normalization of monetary policy.

The increase of the key interest rate to 1%, the highest level of the last 31 years, has not managed to fully stabilize the picture.

At the same time, the central bank continues to buy approximately 2 trillion yen of bonds per month, maintaining a hybrid regime of monetary intervention where tightening and support coexist.

The contradiction is fundamental: if interest rates rise more aggressively, the cost of servicing a debt over 240% of GDP becomes explosive.

If they do not rise, the currency continues to depreciate, reinforcing inflation and eroding confidence.

The fiscal dimension is added to this environment.

The new investment framework promoted under Sanae Takaichi, aiming at the mobilization of approximately 370 trillion yen or approximately 2.39 trillion dollars by 2040 for AI, semiconductors, and strategic sectors of supply chains, reinforces the feeling that the state continues to operate with a logic of perpetual expansion on an already saturated debt.

The risk of contagion for the US economy

The Japanese story, however, is not confined within its borders.

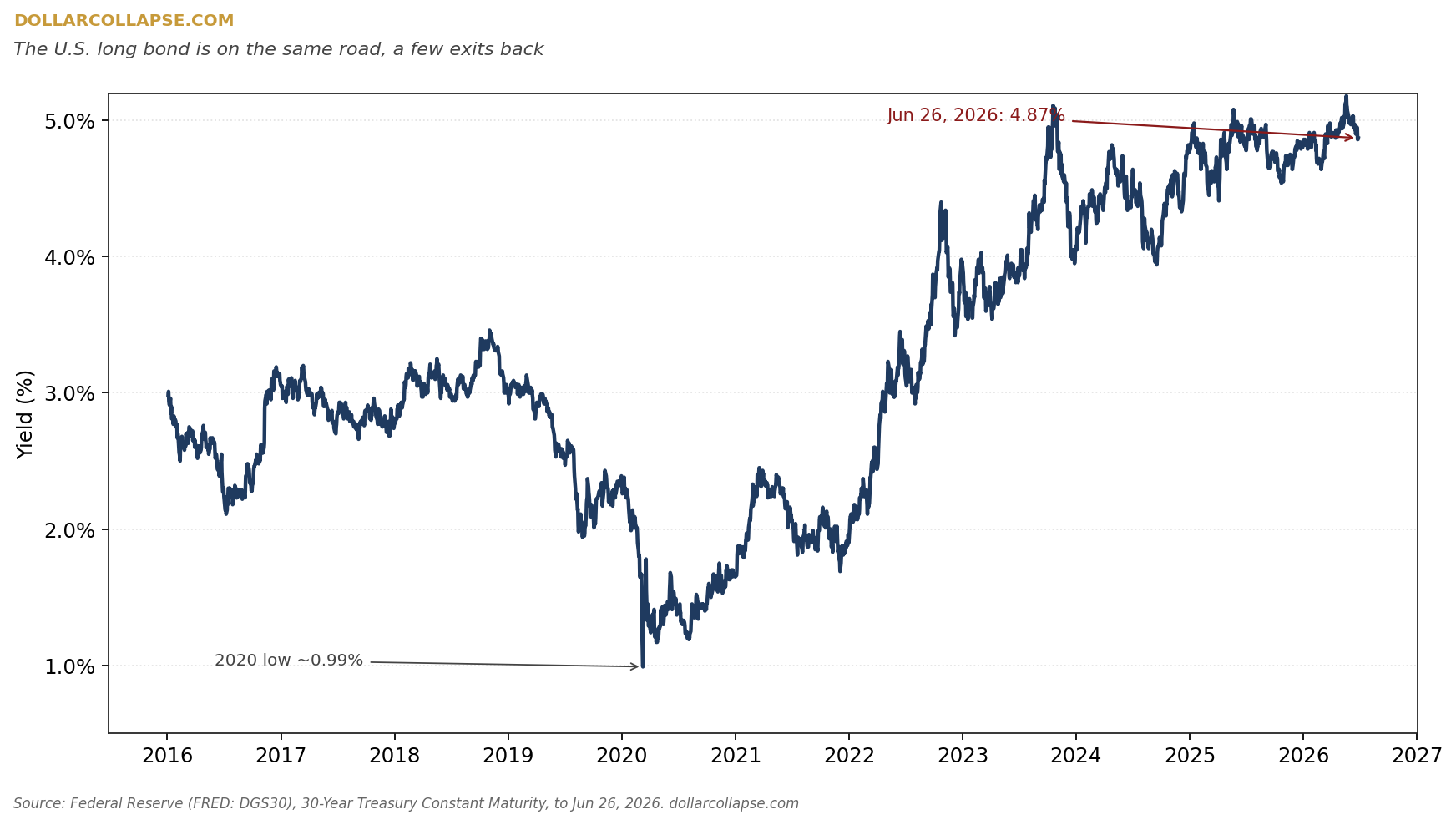

The real point of interest lies in its connection with the United States.

The US finds itself faced with a public debt approaching 40 trillion dollars, while the annual cost of principal and interest payments has already exceeded 1 trillion dollars.

The financing of this system relies on a critical factor: the continuous demand for American government bonds from abroad.

Japan remains one of the largest holders of Treasuries with over 1 trillion dollars.

This means that any pressure on the yen is not simply a local monetary phenomenon, but potentially a factor in the reallocation of capital in the global system.

If Tokyo needs to support its currency for a prolonged interval, the need for dollar liquidity may lead to changes in the composition of its reserves.

A massive liquidation is not required to alter the balance.

In markets of this size, even small variations in net flows can affect the way risk is priced, especially in an environment where American debt issuances remain high and continuous.

The end of risk-free assets

The most critical element, however, is that this interaction between Japan and the US is not direct, but mediated by expectations.

For decades, the fundamental assumption of the markets was that the government bonds of major economies constitute risk-free assets.

What is beginning to be tested is not solvency, but the pricing of this so-called risk-free status.

If this perception begins to shift even marginally, the result will not necessarily be a suspension of payments or otherwise a technical default, but a repricing of the cost of capital on a global scale.

And in this scenario, Japan is not the final point of the horror story.

It is the point from which the crisis is expected to become universal and will concern the whole planet.

www.bankingnews.gr

Readers’ Comments