Optimistic projections from Wall Street regarding the profitability of American corporations are causing concern among an increasing number of top investors and analysts, who warn that an earnings bubble may be forming, capable of threatening the impressive rally of American stocks.

Projections for the earnings of companies in the S&P 500 index are being revised upward at the fastest pace since the post-pandemic recovery period, as the resilience of the American economy and the explosion of investments in artificial intelligence, AI, fuel optimism.

According to data from Bloomberg, analysts predict an increase of approximately 20% to 25% in the earnings of S&P 500 companies over the next twelve months.

This optimism is mainly based on the strong demand for computing power, which favors both semiconductor manufacturing companies and major cloud and artificial intelligence service providers.

However, as the period for announcing second quarter financial results approaches, doubts are intensifying over whether businesses will manage to meet the particularly high expectations of the market.

Many investors express fears that the cost of investments in artificial intelligence is rising at a rapid pace, demand may slow down, while several companies are still struggling to convert their massive investments into substantial and sustainable profitability.

If businesses fail to confirm the highly optimistic forecasts, a significant correction in the stock markets cannot be ruled out.

Ben Inker, head of asset allocation at GMO, characterized the pace of growth in earnings estimates as unprecedented outside of periods of economic recovery following major crises.

As he pointed out, forecasts for corporate earnings for the next two years have increased by nearly 20% in just six months, recording the largest upward revision since 2021.

In his assessment, the market will sooner or later need to adjust to the possibility that these specific forecasts may prove to be overly optimistic.

Similar reservations are expressed by other major investment houses.

Capital Economics warns that earnings expectations linked to artificial intelligence, as well as assumptions about the massive capital expenditures of the sector, may not prove sustainable in the long run.

In the event that these forecasts are revised downward, a broader correction in international stock markets cannot be ruled out.

For his part, Michel Lerner, head of the HOLT investment platform at UBS, estimates that many companies operating in the artificial intelligence value chain are valued as if they can maintain exceptionally high profit margins for many years, something he considers particularly difficult.

Strong corporate earnings continue to support Wall Street

Despite the concerns, corporate results remain the main driver of the rise in American stock markets.

Over the past twelve months, the S&P 500 has gained approximately 20%, while the Nasdaq Composite records a rise exceeding 25%. At the same time, the second quarter proved to be the strongest of the last six years for the main stock market indices.

According to Arun Sai of Pictet Asset Management, the market is going through the strongest cycle of upward corporate earnings revisions since the era of the so-called commodity supercycle of the 2000s.

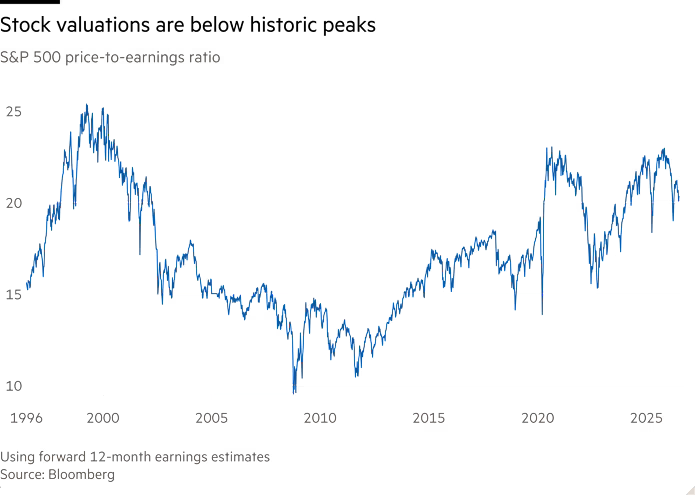

Despite the continuous rise of the indices, valuations of American stocks have not yet reached the extreme levels of previous stock market bubbles.

Today, American stocks are trading at approximately 20 times their expected earnings, a level that is indeed high but lower than that of the pandemic period and noticeably lower than the valuations recorded during the dot-com bubble.

However, Sarah Ketterer of Causeway Capital Management points out that the relatively restrained multiples may indicate that the market is approaching the peak of the profitability cycle, a fact that makes the current juncture less attractive for new investment positions.

At the same time, another factor of uncertainty is the shifting expectations for the monetary policy of the Federal Reserve.

Markets are now pricing in at least one interest rate hike by the end of the year, instead of the two or three cuts they expected at the beginning of the year.

This development increases the borrowing costs of businesses and limits the margins for maintaining current high levels of profitability.

As Kasper Elmgreen of Nordea Asset Management emphasizes, the margin of safety for corporate earnings has now narrowed noticeably and the critical question is for how much longer businesses will continue to positively surprise a market with increasingly higher demands.

www.bankingnews.gr

Readers’ Comments