Markets are facing an unprecedented storm, as a series of interconnected risks threatens to trigger the largest economic shock of the modern era. If the four "black swans" manifest simultaneously, the crash of 2026 could go down in history as a turning point for the global economy. What are the factors driving markets to the brink of the abyss, and why are investors watching developments with growing anxiety? Specifically, according to an article by journalist Martin Wolf in the Financial Times, the global economy remains resilient despite the sharp post-pandemic inflation spike, Donald Trump's tariffs, Russia's war in Ukraine, the war in Iran and, as a result of these two conflicts, major energy crises—the most recent of which is quantitatively the largest in history. "Must the conclusion be that the economy is invulnerable, or just lucky? If it is luck, can it run out?" asks Martin Wolf.

The recent Annual Economic Report of the Bank for International Settlements (BIS) shows that there was indeed resilience, but also luck. Furthermore, it demonstrates that risks are building up, especially in the interaction between fiscal and financial vulnerabilities. To these must be added the social, financial, and other vulnerabilities likely to exist or be exacerbated by the triumphant march of artificial intelligence in the economy. It is not difficult to imagine shocks in which the public sector's capacity to respond effectively is more limited than is taken for granted today. In this context, Martin Wolf examines the impact of certain recent events. Trump's trade war was less damaging than expected on the so-called "liberation day" (April 2, 2025).

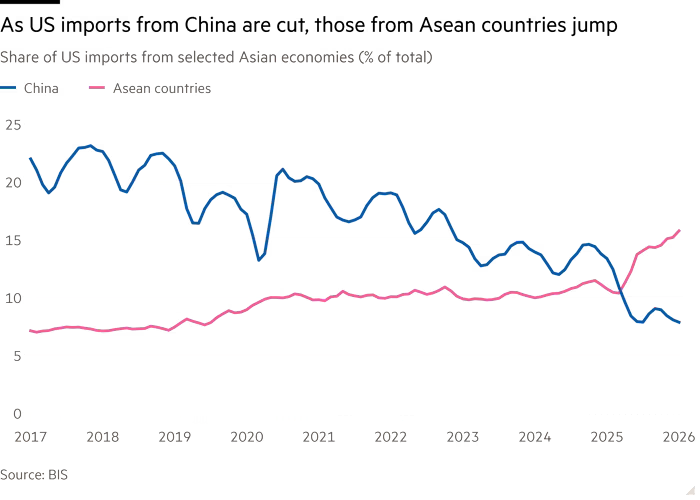

This was partly because tariff levels were ultimately significantly lower than initially indicated, partly because US companies absorbed some of the costs (presumably temporarily) through lower profit margins and, importantly, because the tariffs were highly unequal. The inevitable result was the redirection of trade from direct Chinese exports to the US to exports through other emerging economies (mainly in East Asia) that could produce using Chinese inputs. Furthermore, and critically, the rest of the world did not copy Trump's protectionism. Wisely, it judged that it was too irrational to mimic.

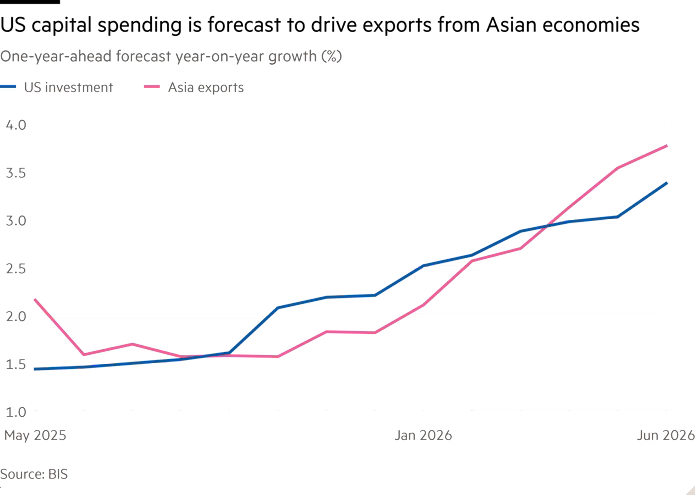

The world also had a very large dose of macroeconomic luck—the artificial intelligence boom. This has triggered not only a boost in confidence in an already overvalued stock market but also a massive surge in domestic investment in the US. This, in turn, had significant secondary effects on the supply of inputs from East Asia. As a result of this boom, along with the aforementioned trade redirection, global trade has remained remarkably strong.

In 2026, however, the global economy suffered another major shock—the reckless attack on Iran. This led to a virtual closure of the Strait of Hormuz, the world's most important transit point for oil, natural gas, and many other critical commodities. This has now lasted for four months and is ongoing. On the supply side, this was the largest oil shock of all time, although stockpiles have mitigated the blow.

If we combine all these points, says the BIS, we see four economic weaknesses, Wolf notes.

First, inflation has risen. The question for central banks is whether this will be brief and transitory or large and long-lasting enough to trigger a new rise in the price level, as occurred with the post-pandemic inflation spike. Could a second shock significantly destabilize inflationary expectations? Yes. Missing the inflation target once may be a misfortune; missing it a second time, even more mildly, would look like negligence.

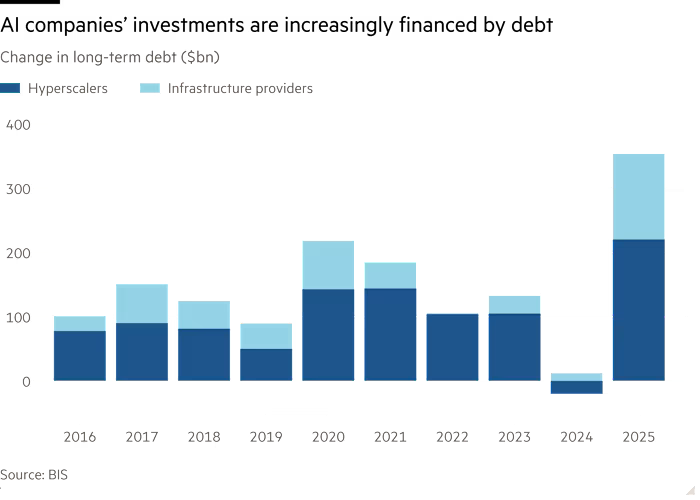

Second, the explosion in spending on artificial intelligence could slow down, perhaps sharply. One reason may be the intense public backlash against the technology. In the long run, the combination of fierce competition with disappointing returns could lead to an investment collapse. This, the BIS notes, has happened before in innovation-driven investment booms.

Third, today's loose financial conditions could tighten abruptly, as a result of a traditional panicky market reaction. Compressed risk premiums, rising leverage, and, not least, the rapid growth of a relatively opaque and unregulated non-bank financial intermediation sector are being observed. Note also that private debt is not far from 2007 levels.

Fourth, governments in high-income countries are losing control of their public finances. With few exceptions, they run large structural fiscal deficits, while average public debt-to-GDP ratios are at levels not seen since World War II. These countries, particularly in Europe, also face the challenges of high energy prices and an aging population. Interest rates, both nominal and real, are at levels not seen since before the global financial crisis. As Manoj Pradhan and Charles Goodhart argue in The Unanchored Central Banker, the days of low inflation and near-zero interest rates are in the past.

Beyond the above, the Bank for International Settlements (BIS) highlights the interaction of sovereign defaults with public debt markets. Specifically, it emphasizes the growing role of hedge funds in financing governments. Their strategy relies on high leverage. This increases the risks of panic, in which positions are liquidated at a very high speed. We saw such disruptions at the beginning of the pandemic and again in the United Kingdom in September 2022.

For central banks, all of this combined threatens to cause significant trouble. One risk is fiscal shocks, which, as the BIS emphasizes, are also likely to reduce the flexibility margins of monetary policy. Furthermore, any disruptions in financial markets are likely to be met with strong support from the authorities. But this is certain to further increase moral hazard. The current shift toward procyclical financial deregulation enhances the likelihood of this risk even further.

Finally, there is the new "bête noire" of the BIS: stablecoins, which are intended by some to be equivalents of money, but in any crisis, they will not be.

Summarizing, Martin Wolf states: "The global economy is resilient partly because it had luck. Luck is running out. If the economy is to remain resilient, it must become fundamentally more resilient. Achieving this is now a priority."

www.bankingnews.gr

Readers’ Comments