The global economy is walking blindly toward absolute catastrophe, trapped in an unprecedented illusion of growth that is sustained exclusively by the toxic debt of Artificial Intelligence. As household savings collapse and tech giants "secretly" load up on trillions, the countdown to the most violent crash in history has already begun. The abrupt closing of the credit tap will be the final blow that will plunge the planet into a biblical, irreversible recession.

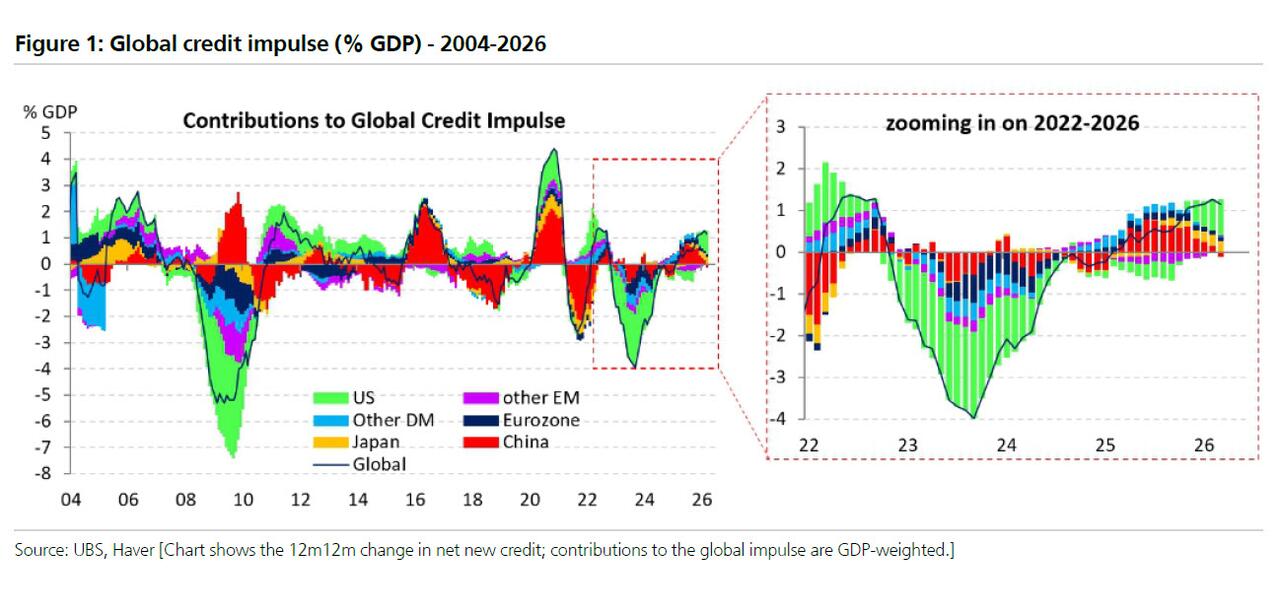

What the credit pulse signals

Not long ago, something remarkable happened: while China had consistently led the growth of the global "credit impulse" in recent years—defined as the change in net new credit as a percentage of GDP and a useful indicator of real domestic demand—there has now been a dramatic shift in the balance of credit creation. According to UBS calculations, the global credit impulse is now primarily an American affair: +2.6% of GDP, meaning approximately $800 billion in additional credit over the past year, much of which is linked to financing various Artificial Intelligence (AI) projects. At the same time, Beijing plays a secondary role in global credit creation, with the US now accounting for more than half of the global credit impulse, primarily due to the continuous expansion of lending fueled by capital expenditures (capex) for AI. We remind you that hyperscalers alone are expected to issue $600 billion in debt in 2026.

The obvious consequence is that if this AI-linked credit "firehose" is abruptly shut off, the most important engine of the global credit impulse will reverse, likely pushing the global economy into recession.

Something has changed

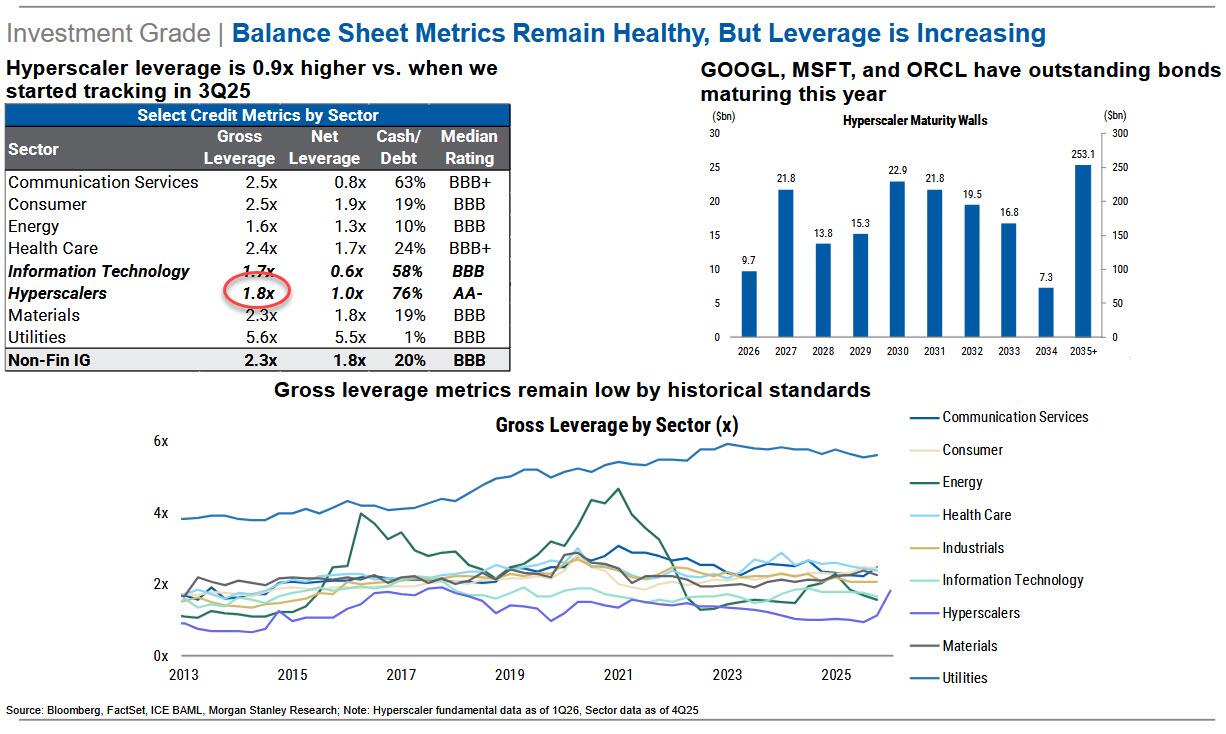

At the same time, Bloomberg reached the same conclusions, writing that "something big just changed in the American economy." In other words, "the US economy is abandoning the long period of deleveraging that followed the 2008 financial crisis and is moving to a model based much more on debt." This dramatic re-leveraging of the American economy also forms the basis of the latest weekly note from SocGen strategist Albert Edwards. However, instead of focusing solely on the relentless increase in corporate debt financing the investments of hyperscalers—who, according to Morgan Stanley calculations, have doubled their gross leverage ratio in just two quarters, from 0.9x to 1.8x, a pace that could soon turn AI debt into a debt bubble (if it isn't one already, as we warned last October).

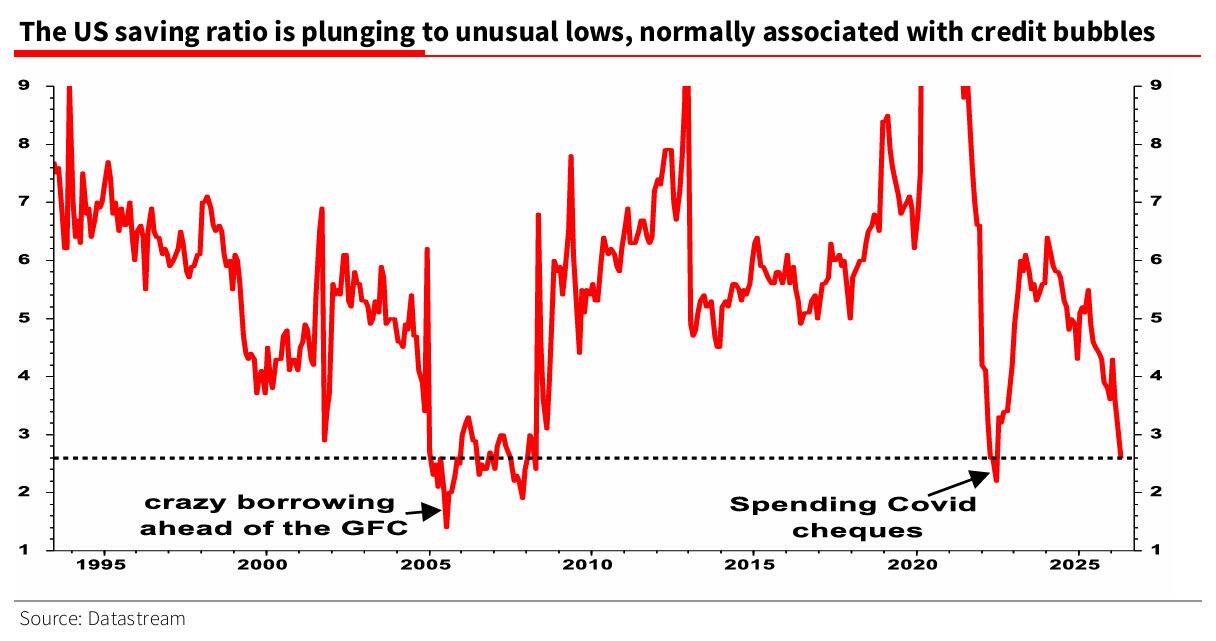

the SocGen strategist points out that "much less attention is paid to the explosion in American consumer lending, which is clearly reflected in the collapse of the household savings rate to unusually low and likely unsustainable levels (2.6%)." This is a development we highlighted just a month ago.

According to Edwards, the immediate boost the economy receives from increased business and household lending—for investment and consumption, respectively—is obvious. However, there is another dimension that, as he warns, is particularly important for monetarists: the potential impact on inflation from the rapid increase in the money supply. At the same time, there is also the issue of liquidity.

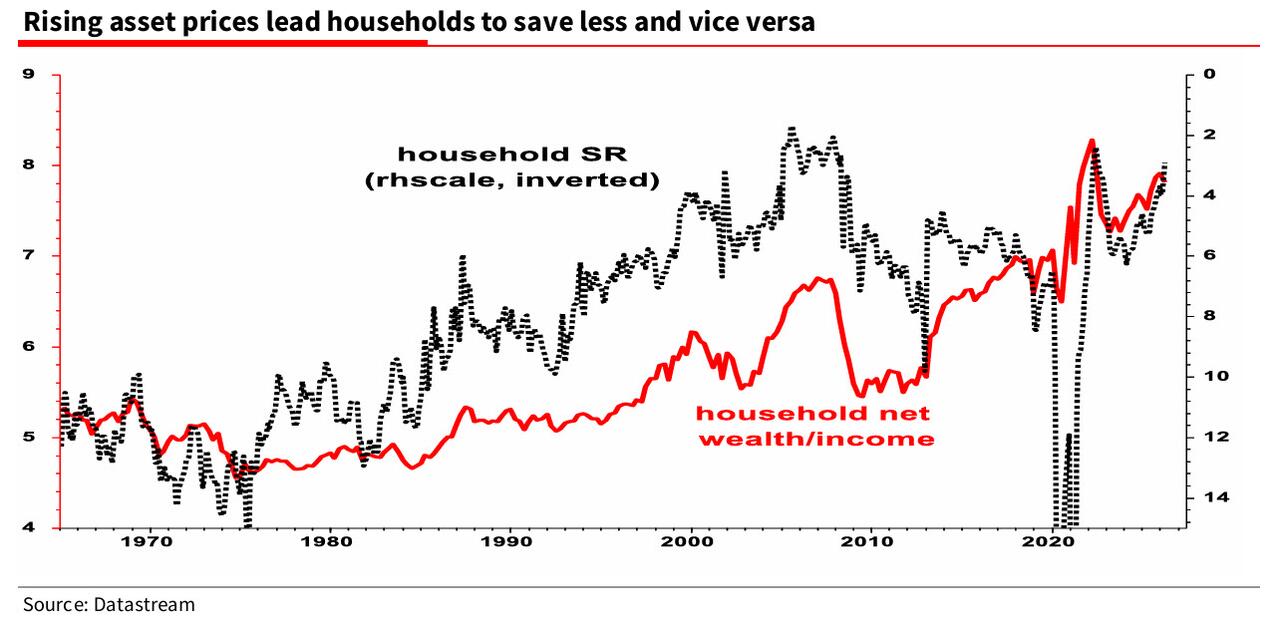

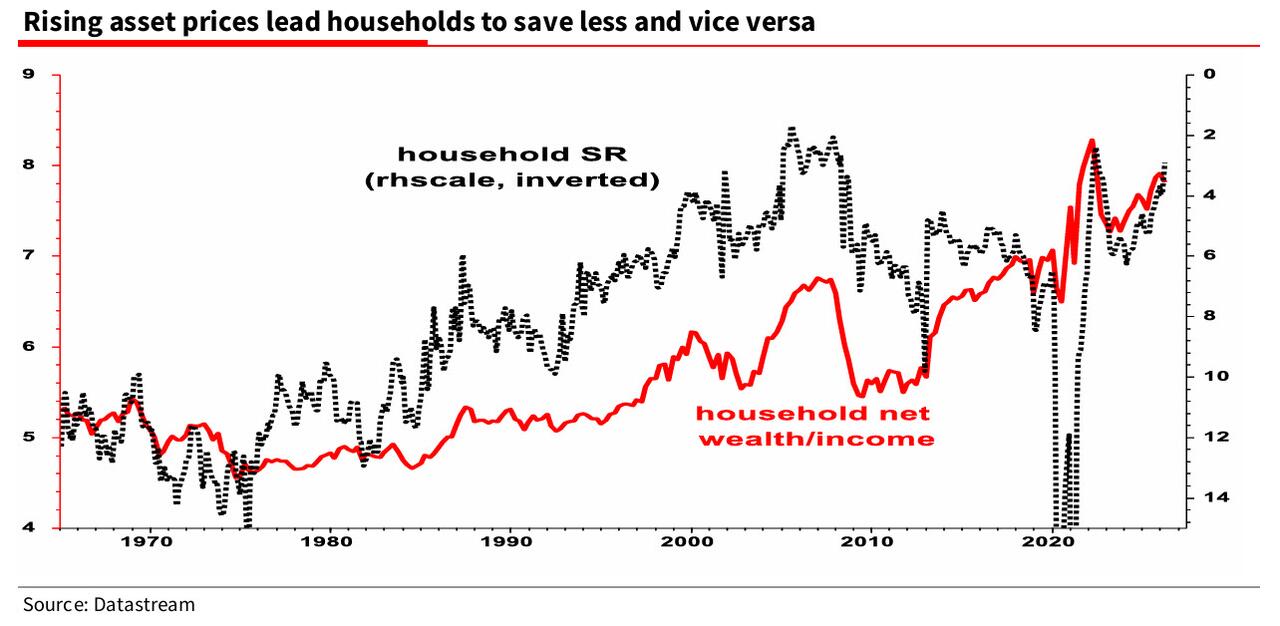

In other words, if households and businesses are now following the public sector in increasing their net borrowing to fund spending in the real economy ("things"), they may be absorbing liquidity from financial markets and channeling it into the real economy. This could threaten asset valuations, perhaps signaling a reversal of the long-standing phenomenon of "secular stagnation"—that is, excess savings relative to investment. Perhaps, Edwards wonders, the recent decline in precious metals and cryptocurrencies reflects precisely these tighter liquidity conditions in financial markets. Returning to the collapse of the personal savings rate, Edwards warns that for someone who is not an economist, it is difficult to grasp exactly what is happening when looking at a chart of the savings index. The following chart clearly shows that the American consumer today resembles the character Wile E. Coyote: they run past the edge of the cliff and remain suspended in the air for a moment before finally collapsing.

In other words, if households and businesses are now following the public sector in increasing their net borrowing to fund spending in the real economy ("things"), they may be absorbing liquidity from financial markets and channeling it into the real economy. This could threaten asset valuations, perhaps signaling a reversal of the long-standing phenomenon of "secular stagnation"—that is, excess savings relative to investment. Perhaps, Edwards wonders, the recent decline in precious metals and cryptocurrencies reflects precisely these tighter liquidity conditions in financial markets. Returning to the collapse of the personal savings rate, Edwards warns that for someone who is not an economist, it is difficult to grasp exactly what is happening when looking at a chart of the savings index. The following chart clearly shows that the American consumer today resembles the character Wile E. Coyote: they run past the edge of the cliff and remain suspended in the air for a moment before finally collapsing.

A worrying way

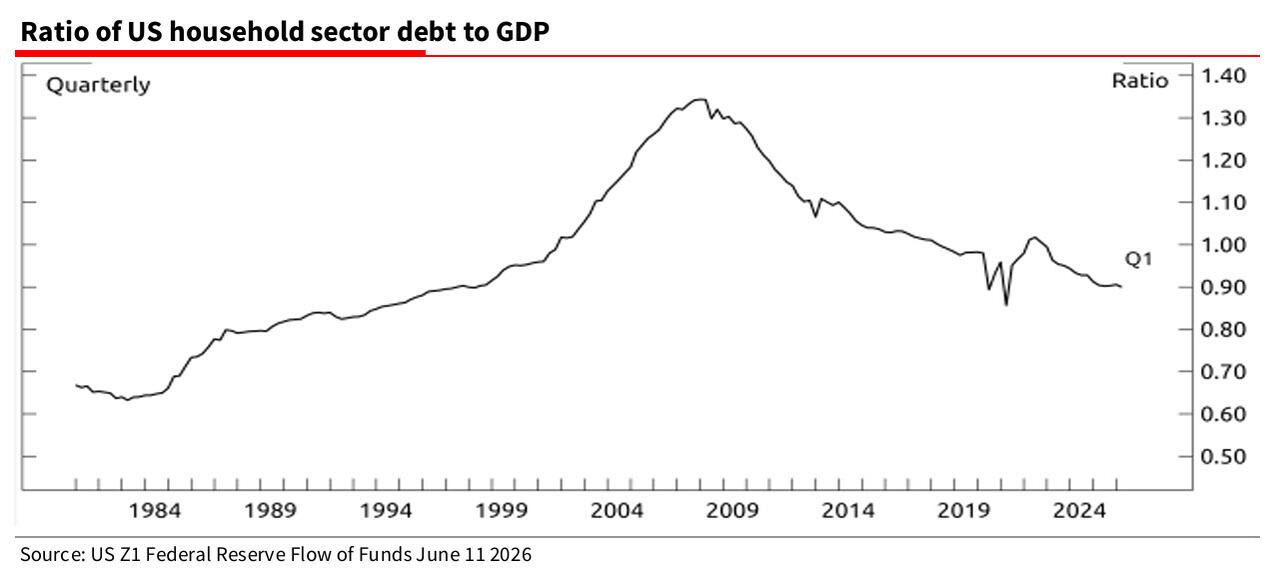

A more worrying way to visualize this is to observe that all key indicators of real income are shrinking year-over-year (YoY). You don't need to have a doctorate in economics to understand that if the Saving Ratio (SR) in the US stops declining, consumer spending will only grow as long as income grows... which is currently falling. And woe to the economy if, as Edwards assumes, the savings index returns at some point to more normal levels around 5% or higher—about double today's. (An optimistic counter-argument is that US households have been deleveraging since the 2008 financial crisis and are in relatively good shape, so there is no reason for panic.) Certainly, the household balance sheet may look healthy, but the only reason consumption continues to grow by about 2% year-on-year is that households feel wealthier (thanks to the wealth effect created by the stock market rally) and therefore believe they can save less. As often happens in any stock market bubble, a rise in asset prices that may later prove temporary (or lead to another Fed bailout) has caused a sharp drop in the savings index. As we found in 2008 (and in other cases), Edwards observes, this all works fine until asset prices start to fall. Then the savings index shoots back up, as it did immediately after the COVID shock, when the savings rate temporarily exceeded 30%, forcing the government and the Fed to print money aggressively. That is why Edwards concludes that "both consumption and investment depend on the Artificial Intelligence (AI) bubble not bursting".

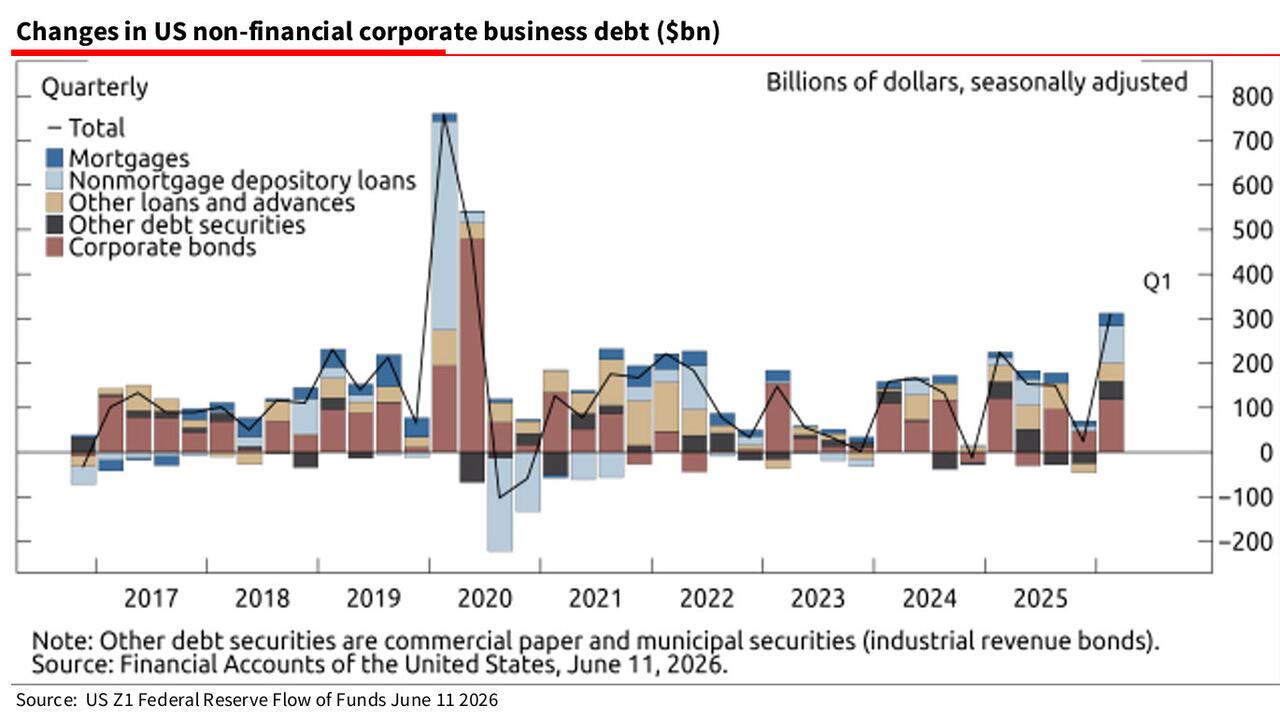

If the AI-fueled credit "firehose" is abruptly shut off, the biggest lever of global credit impulse will reverse and likely push the global economy into recession. In other words, AI now holds "hostage" not just the stock market, where the 10 largest companies are responsible for almost all S&P growth this year, but the economy itself. And all of this depends on whether investors will continue to avoid difficult questions about the several trillion dollars in off-balance-sheet liabilities reported yesterday. And of course, as we have been persistently pointing out for a year, since we emphasized that AI is now also a debt bubble, corporate borrowing is also increasing at a rapid pace, mainly for purposes related to AI. (The Fed included a detailed analysis of recent lending trends in the latest Z1 Flow of Funds report published last week.)

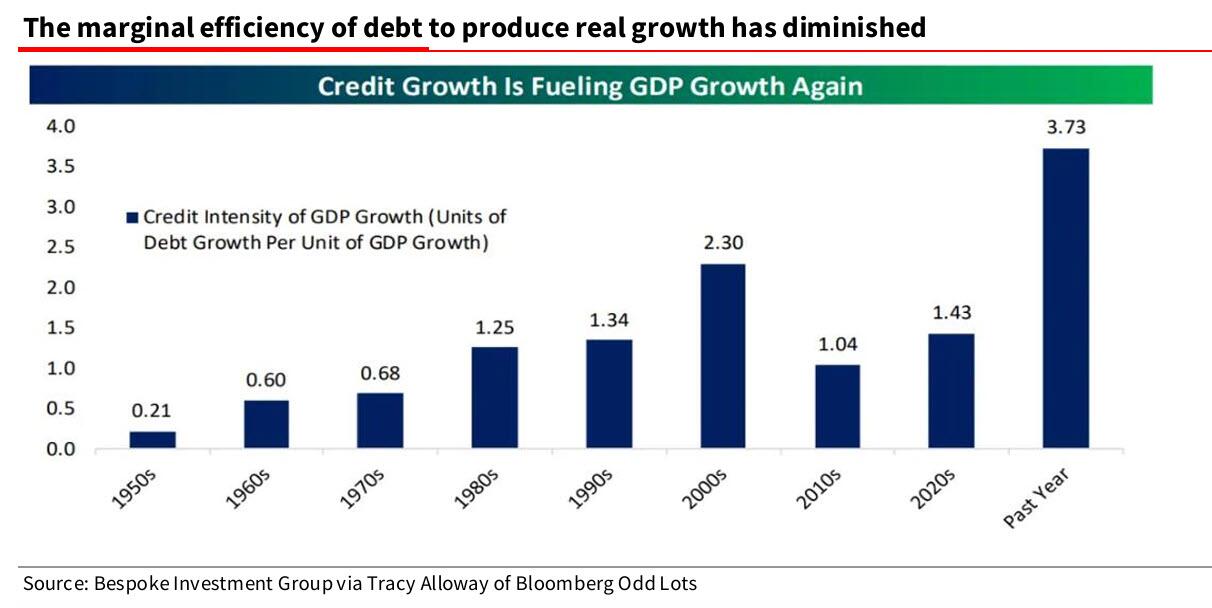

A final observation: yes, the US is now leading the world in credit impulse, but even so, a huge amount of new debt is required to produce one additional unit of GDP.

This makes the economy even more vulnerable in case investors start to doubt the "pot of gold at the end of the rainbow" of AI. Edwards concludes with the same warning we have been repeating for months: "Watch this over-indebted space carefully."

www.bankingnews.gr

Readers’ Comments