Large economic crises rarely begin with an explosion.

They are not always accompanied by bank closures, stock market crashes, or dramatic central bank interventions.

They often begin quietly, almost imperceptibly, through small shifts that initially look technical or insignificant.

Until the moment it is realized that the old order of things has already begun to dissolve.

This is exactly what is happening today in the global monetary system.

For the first time since the end of World War II, the dollar is no longer treated as the sole and unquestionable foundation of the international economy.

It is not a collapse yet.

It is, however, a gradual erosion of trust that is spreading from the largest economies of the world to the central banks of emerging markets.

And the data is now so extensive that it can hardly be considered a coincidence.

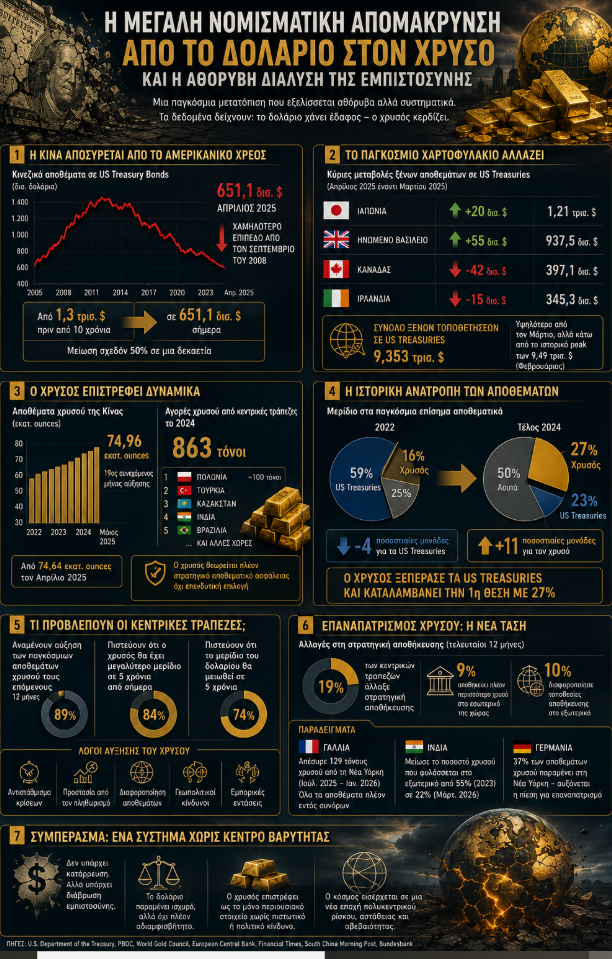

China is gradually abandoning American debt

The first and perhaps most worrying sign comes from China.

According to the latest data from the American Department of the Treasury, Chinese holdings of American government bonds decreased in April to 651.1 billion dollars from 652.3 billion in March.

At first glance, the reduction seems negligible.

However, the real news lies elsewhere.

The current level is the lowest since September 2008, that is, from the period of the collapse of Lehman Brothers and the largest financial crisis of recent decades.

Ten years ago, China held American bonds worth over 1.3 trillion dollars.

Today, the amount has almost halved.

This reduction is not the result of panic.

It is the result of strategy.

Beijing is not selling aggressively.

It is not causing turmoil in the markets.

It is steadily and systematically reducing its dependence on the American financial system, preparing the ground for an era where the dollar may not constitute the sole point of reference for international trade.

This slow decoupling is perhaps more dangerous than a violent flight, because it reveals long-term planning.

The global system of foreign exchange reserves is fragmenting

On an aggregate level, foreign placements in American bonds still amount to 9.35 trillion dollars.

This size remains huge.

However, behind the total number hides a deep change in behavior.

Japan increased its reserves to 1.21 trillion dollars.

The United Kingdom strengthened its placements to 937.5 billion.

At the same time, Canada reduced its placements by more than 42 billion dollars within one month, while Ireland also continued to limit its exposure.

This picture reveals something deeper.

There is no longer a common strategy.

There is no longer consensus around what is the safest way to manage foreign exchange reserves.

Each country is building its own defense against an uncertain future.

And when a global system ceases to operate under common assumptions, it begins to lose its cohesion.

Gold returns to the spotlight for the first time in decades

The most impressive element of the change is the explosive return of gold.

The People's Bank of China increased its gold reserves for the 19th consecutive month in June 2026.

Chinese reserves now amount to 74.96 million ounces.

The fact that purchases continue despite historically high prices has special significance.

Central banks do not buy gold because they consider it cheap.

They buy it because they consider it safe.

In 2024, central banks bought 863 tons of gold.

Poland alone bought about 100 tons.

Turkey, Kazakhstan, India, Brazil, and dozens of other countries followed.

This is one of the largest waves of gold purchases in the history of the post-war period.

The historic reversal that worries the markets

The European Central Bank recorded a development that a few years ago would be considered unthinkable.

The share of American government bonds in global reserves decreased by four percentage points within just two years.

During the same period, the share of gold increased by eleven percentage points.

The result was historic.

At the end of the previous year, gold represented 27% of global official reserves and surpassed American bonds for the first time.

In other words, the central banks of the planet trust an interest-free metal more than the debt of the strongest economy in the world.

This is not simple rebalancing.

It is a vote of no confidence of historical character.

89% of central banks seek to acquire even more gold

The latest survey by the World Gold Council is revealing.

89% of central banks expect a further increase in global gold reserves within the next twelve months.

Even more impressive is that 84% consider that on a five-year horizon, gold will occupy a larger share in foreign exchange reserves than today.

At the same time, 74% of participants estimate that the share of the dollar in global reserves will decrease within the next five years.

These numbers do not constitute a simple investment forecast.

They constitute a collective assessment of the very custodians of the global monetary system.

The new trend: gold repatriation

The crisis of trust does not concern only what central banks buy.

It also concerns where they store it.

19% of central banks changed their gold storage strategy within the last twelve months.

The percentage is almost four times higher compared to a year ago.

France withdrew 129 tons of gold from the vaults of the Federal Reserve in New York and now keeps the entirety of its reserves within French territory.

India reduced the percentage of reserves it maintains abroad from 55% in 2023 to just 22% in 2026.

In Germany, political pressure is rekindling for the return of an even larger part of the reserves from New York.

These are developments that a decade ago would be considered unthinkable.

The global economy is entering an era without an anchor

The most worrying element is not that central banks are buying gold.

It is that they are preparing for a world without an absolutely safe haven.

The dollar remains dominant.

But it is no longer considered invulnerable.

Gold is regaining its position.

But it cannot replace the international monetary system on its own.

The result is the creation of a multipolar world without a common center of gravity.

And history shows that transitional periods between two monetary eras are usually the most dangerous.

There is no collapse yet.

There is no panic.

There is no financial shock.

There is, however, a slow, persistent, and extremely worrying shift in global trust.

And when the central banks of the world begin to prepare for the possibility that the current system might not last forever, then the real crisis has already begun, it has just not yet become visible to most.

www.bankingnews.gr

Readers’ Comments