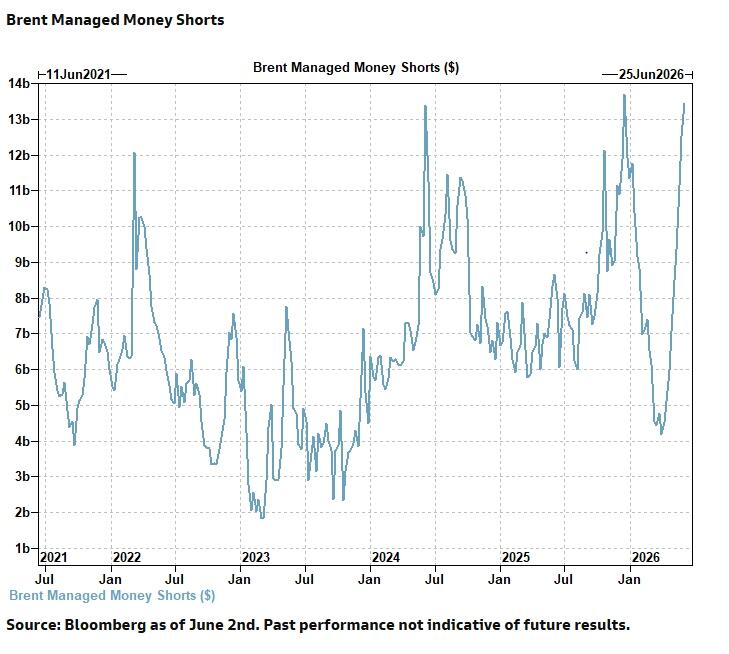

In yet another sign that the oil market may be overly complacent regarding the scale of the supply disruption in the Middle East, traders are increasing their short positions in oil futures.

The global economy is moving on shifting sands, even as international markets insist on keeping their eyes shut. Although there is talk of a potential US-Iran agreement, the situation regarding oil inventories is evolving into a thriller that threatens to blow up the economy. The reality is nightmarish, as the global market has already lost an unimaginable 13 million barrels per day, with the Strait of Hormuz in a state of "cardiac arrest." At the same time, traders on the stock exchanges, trapped in an unprecedented delusion of complacency, continue to bet on falling prices.

Traders are shorting as if Hormuz is open

In yet another sign that the oil market may be overly complacent regarding the scale of the supply disruption in the Middle East, traders have been increasing their short positions in oil futures for the better part of the last two months. Since the beginning of April, portfolio managers have been increasingly betting on a decline in oil prices, according to the latest available Commitment of Traders (COT) data from exchanges through June 2. Brent short positions tripled between the end of March and early June, according to data compiled by energy analyst John Kemp.

By June 2, Brent short positions had surged to their highest level since January, when the US arrested Venezuelan leader Nicolas Maduro, and the market expected increased supply from Venezuela in the coming months. The vertical increase in short positions and the weeks-long sell-off of long positions over the past eight weeks suggest that traders are betting on a swift restoration of supply.

The oil market is based on hopes, expectations, emotions, and fears, and the sum of all these at the moment seems to be that the community of hedge funds and portfolio managers is reluctant to bet on a summer with real physical supply shortages. However, the market may soon be confronted with the reality of shrinking global inventories, including in the United States, where stocks at Cushing (the delivery point for WTI crude) are just weeks away from falling to minimum operating levels.

Excessive noise surrounding the ceasefire, which is tested almost daily with one strike or retaliatory response after another, does not help the paper market, which may have become too detached from the magnitude of the supply loss. Traders react to every signal of an "imminent deal" with liquidations, only to start buying oil futures again when Israeli strikes in Lebanon, US "self-defense" strikes in Iran, or Iranian strikes on regional infrastructure threaten to blow up the fragile ceasefire. All this time, investors in the oil market continue to hope for an imminent resolution and the reopening of the Strait of Hormuz, which would flood the market with oil. And this has been their hope for three and a half months.

The issue is that even a full reopening of the Strait would not lead to immediate relief for buyers. First, shipowners and ship managers would need guarantees that they won't be caught by surprise again with stranded tankers. Then, oil cargoes would need weeks to reach buyers—weeks that the market may not have during the peak summer demand period. The world has lost about 13 million barrels per day (bpd) of oil supply, the International Energy Agency (IEA) reported in its May oil market report. "Rising supply losses from the Strait of Hormuz are draining global oil stocks at a record rate," the IEA reported, adding that observed global inventories, including oil on tankers at sea, fell by 250 million barrels during March and April, or 4 million barrels per day. Sooner or later, volumes of oil at sea and onshore inventories will run dry, leaving demand destruction as the only buffer to hold back oil price spikes.

Furthermore, extreme price volatility and the noise regarding a deal that is "coming at any moment" are sidelining part of the trading community. "Participants continue to remain on the sidelines, given the liquidity, uncertainty, and the headline-driven nature of the market," ING commodity strategists Warren Patterson and Ewa Manthey said in a note on Wednesday. "This is reflected in the total open interest in ICE Brent, which has continued to trend lower and is at its lowest level since August 2025."

Many traders have been shorting oil since April in the hope that the ceasefire and negotiations would yield a peace agreement before the world ran out of buffers to offset the bulk of the supply disruption. "Safety stocks and shock absorbers are steadily declining, and the market's ability to absorb this imbalance is drastically reduced today compared to where we started and the coming weeks," said Chevron CEO Mike Wirth at the Bernstein 42nd Annual Strategic Decisions Conference in late May. "It is likely that we will see these pressures pass through more directly to physical product prices, and there are more upward pressures that I would expect as we head into June and certainly through July." According to the ING strategists' note, "With no deal in sight and with the global oil market tightening significantly every day, we see an upward path for prices, particularly if these disruptions extend into the third quarter, a period of seasonally stronger oil demand."

www.bankingnews.gr

Readers’ Comments