The sharp drop in the Nasdaq on Friday, 6/5, felt like the first crack in a narrative that until recently seemed invulnerable: that artificial intelligence is not just a useful tool, but a power capable of transforming civilization, a technological leap of such magnitude as to justify valuations similar to those of 1999 for dreams that also resemble 1999. Technology stocks led the largest market correction since October, with tech giants linked to artificial intelligence losing hundreds of billions of dollars in market value in a single session. One of the main catalysts was the stronger-than-expected US employment report, which reignited fears of interest rate hikes by the Federal Reserve (Fed) and caused concern even for President Trump. Another factor was Broadcom's weak forecasts.

The same microchip manufacturing companies and large cloud computing providers that had fueled the impressive upward rally of the last year, such as Nvidia and the so-called hyperscalers, were the day's biggest losers. Investors began to question whether the artificial intelligence boom could continue to justify "bubble-like" valuations without the prospect of immediate interest rate cuts. However, a small group of analysts and investors, as well as JPMorgan CEO Jamie Dimon and Bridgewater Associates founder Ray Dalio, had already warned in previous days and weeks that something didn't feel right.

"One more reason why 2026 looks like 1999"

On June 3, two days before the market drop, Owen Lamont, a senior portfolio manager at Acadian Asset Management, published an article on his blog, Owenomics, titled "A pessimistic approach to optimistic growth forecasts." He argued that the clearest sign of a bubble is not necessarily the price trend, but the surge in expectations for future earnings used to justify those prices. He even presented his data.

According to his calculations, from 1985 to today, analysts have predicted an average annual earnings growth of about 13% for S&P 500 companies, while the actual growth was closer to 7%. Citing research by Pedro Bordalo, Nicola Gennaioli, Rafael La Porta, and Andrei Shleifer, he argued that strong earnings performance creates "irrational exuberance" among investors, who tend to project this good performance indefinitely into the future. "Their findings suggest that shareholders will likely be disappointed over the next five years, as earnings will not grow as fast as expected, just as happened after the tech stock bubble," he wrote.

Citing well-known analyst Ed Yardeni, who coined the term "bond vigilantes," Lamont noted that expectations for long-term earnings growth of the S&P 500 reached 20.2%, surpassing even the 2000 high of 18.6%. "Perhaps," Lamont wrote, "when we reach 2031, we will look back and consider today's valuations yet another confirmation of the efficient market hypothesis. However, for me, today's optimism is one more reason why 2026 looks increasingly like 1999." From his perspective, the risk is not so much that the S&P 500 is "too high" in some abstract sense, but that investors and analysts are repeating the familiar mistake of excessive optimism and exaggerated expectations.

An economy with diverging trends

Two days earlier, on June 1, David Kelly, Chief Global Strategist at JPMorgan Asset Management, published his weekly note titled "Investing in an economy with diverging trends." He described a scenario that, at first glance, seemed reassuring: real US GDP growth between 2.0% and 2.5% in 2026, a slowdown to 1.5%-2.0% in 2027, unemployment slightly below 4%, and inflation receding back toward 2% over the next year. However, as he pointed out, these averages hide "the many different and diverging trends evolving today in the American economic landscape." These include:

-

Rich vs. Poor: Based on the work of Thomas Piketty and Emmanuel Saez, Kelly noted that the top 10% of American households received about 50% of total income in 2022. Federal Reserve data show they held about 62% of household assets, while the total value of household assets amounted to about 630% of GDP—levels higher than those before the dot-com bubble or the 1987 crash.

-

Technology vs. the rest of the economy: The 10 largest companies in the S&P 500 index, eight of which are essentially tech companies, now account for over 41% of the index's market capitalization and 33% of its earnings. In the year to the first quarter, real GDP grew by 2.6%, but real investments in equipment and R&D grew by 8.9% and 9.3% respectively, due to the boom in capital expenditures by hyperscalers. Kelly cited estimates that these expenditures (capex) will skyrocket by 78% in 2026, from $416 billion to $739 billion.

-

Perception vs. reality: Even when stock indices were hitting record highs in late May, consumer confidence, as measured by the University of Michigan, fell to a record low.

Meanwhile, a "misery index," resulting from the sum of unemployment and inflation, although at its worst level in over three years, remained better than it had been for more than half the time over the last 50 years. He also shared a personal story that summarizes the "two Americas" and the enduring reality that Wall Street is not the same as Main Street. As he said, in mid-May he and his wife took a road trip along the East Coast, reaching Charleston and returning through the Appalachian Mountains. At a stop at a Jersey Mike's, they met a man in line who had just found a job after five months of searching.

"He wanted to celebrate by buying two big sandwiches — one for that night and another to put in the fridge for the next day." A week later, they couldn't visit one of their favorite Italian restaurants in downtown Manhattan. "We had forgotten to book a table earlier in the week and there was no chance of finding a reservation for that night," he wrote, noting that OpenTable reservations were up 13% year-on-year in May. "It's the story of two different restaurants and another example of the diverging trends shaping today's economic and financial environment," he concluded, adding that "as divergences increase across multiple dimensions, so do the risks of something going seriously wrong."

Wall Street's optimistic base scenarios

While Kelly and Lamont strengthened their warnings, some of Wall Street's most influential research firms were publishing forecasts that, depending on the perspective, confirm their argument. On June 1, the same day as Kelly's note, Deutsche Bank's global economic analysis team published its World Outlook report, describing 2026 as "anything but boring" and characterizing the year as "1999 meets 1990, but hopefully not 1973" — a collision between the optimism fueled by artificial intelligence and an energy shock in the Middle East. The bank reiterated its target for the S&P 500 at 8,000 points by year-end and a price-to-earnings (P/E) ratio around 25x. Its economists estimated that S&P 500 earnings per share (EPS) will grow by 14.2% in 2026, supported by strong performance in the technology and financial sectors, as well as "sustained high valuations."

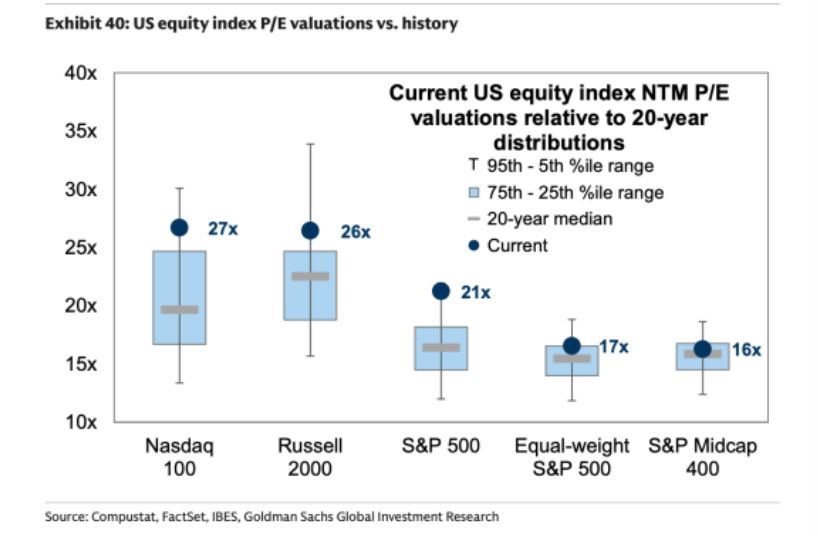

Four days earlier, on May 29, Goldman Sachs' US portfolio strategy team raised its 2026 forecast for gross proceeds from US IPOs to $225 billion, up from $160 billion previously. At the same time, it estimated that total US corporate equity issuance, including secondary offerings and convertible securities, would reach $675 billion, about 1% of the Russell 3000 index's capitalization. Goldman Sachs also set a 12-month target for the S&P 500 at 8,300 points, implying a forward P/E ratio near 21x. The bank's valuation charts showed that major US stock indices are trading in the top quartile of their last 20 and 30-year valuations, with the Nasdaq 100 at the top of this scale. Both banks were careful to qualify their outlooks, avoiding extreme bullish predictions.

Deutsche Bank pointed to the risk of higher inflation and slightly elevated long-term interest rates, while Goldman Sachs acknowledged that the pace of stock buybacks is slowing as investments in AI and capital equipment skyrocket. However, through Lamont's lens, these forecasts fit a familiar pattern: base scenarios that rely on maintaining double-digit earnings growth, high valuations, and an investment explosion around artificial intelligence that never meets serious obstacles. Jamie Dimon and Ray Dalio do not seem to share this optimism with the same certainty.

"Everything running at full throttle"

Speaking on May 27 at the Bernstein Strategic Decisions Conference, Jamie Dimon gave a blunt description of what he sees from the front lines of the banking world. "Everything is running at full throttle, my friends," he said. "Deals are proceeding nonstop, bankers are busy, private equity sponsors are spending. Clients are not hesitating." He estimated that mergers and acquisitions (M&A) are heading for their best year in recent times, while activity in equity capital markets—IPOs and secondary offerings—will be "huge."

In the week that followed, Anthropic confidentially filed for an IPO, Goldman raised its IPO forecasts, and SpaceX officially filed for a public listing. Dimon then used a word with heavy historical baggage, the same one Lamond had used. "There is a lot of euphoria out there," he said, echoing the famous phrase "irrational exuberance," which former Fed Chair Alan Greenspan had coined in 1996. For critics, of course, this is not just "irrational exuberance," but a bubble mentality. Dimon based his concern on four specific years: 1972, 1986, 2000, and 2007. As he noted, each was a period of high confidence, intense business activity, and a general belief that fundamentals justified the optimism—just before the music stopped. The 1973–74 bear market destroyed the stocks of the so-called "Nifty Fifty."

The "Black Monday" crash of 1987 and the savings and loan crisis followed the euphoria of the early Reagan years. 2000 marked the peak of the dot-com bubble, while 2007 was the final year before the global financial crisis. Dimon's worry, as he said, is not that economic activity isn't strong, but that when something "seems to be going very well," problems often lurk around the corner. Dimon also pointed to the role of fiscal policy, estimating that $10 to $12 trillion in deficit spending over six or seven years has mechanically boosted corporate earnings and demand. The risk, according to him, is that markets treat this boost as organic economic strength rather than a temporary "sugar hit." "The government borrows money and gives it to people, and that money is spent," he said. "This also fuels corporate earnings. It doesn't automatically mean all companies suddenly became geniuses."

Dalio and the ghost of 2000

On June 3, the day Lamond's note was published, Dalio told Bloomberg Television that his own bubble indicators, which track investor sentiment, market concentration, and valuations, show that US stock markets are "approaching, without having yet reached, the levels of 2000 and 1929." Dalio emphasized that the creation of a bubble and its bursting are two different events.

The "pricking" of the bubble, he argued, usually happens when investors need to convert wealth that exists on paper into real money, selling assets to pay debts or taxes. "You cannot spend wealth," he said. "You must sell wealth to get money, because only money can be spent." Goldman Sachs has an internal skeptic who has been expressing a pessimistic view on artificial intelligence for years. James Covelloh, the bank's head of global equity research, questioned the direction of the markets on the Goldman Sachs Exchanges podcast on Tuesday, June 2. As he said, the fundamental question remains the same. "At some point, you have to make money," he declared. "You make investments in a business to generate returns and profits. And for the last two years, we have been moving away from that goal instead of approaching it."

Covelloh recalled that in a 2024 research report, he had estimated it would take 18 months to two years to see if the massive wave of capital flowing into AI infrastructure would yield returns commensurate with the spending. As he told colleagues Alison Nathan and George Lee, this time limit has already been passed and it still hasn't happened. George Lee, co-head of the Goldman Sachs Global Institute, appeared more optimistic about the long-term prospects of AI and estimated that $7 to $8 trillion would eventually be spent globally on related infrastructure.

He argued that simply "displacing" existing sources of profitability is not enough to justify such levels of investment. The math only works if AI creates significant new economic activity. So far, however, data on return on investment (ROI) in businesses remain disappointing. "I truly believe it all comes down to one thing: are businesses earning or saving money by implementing artificial intelligence?" said Covelloh. "If so, then this technology will fulfill its promises."

The "shadow blog": "The Token Bill is coming"

The skeptics are already out there, arguing that the return on investment (ROI) is simply never going to come and that a… 1999 moment is much more to be feared than many want to admit. "When the bubble bursts," software engineer Benjamin Horne wrote on his Substack on June 3, "Paul Kedrosky, Ed Zitron, and Gary Marcus will have the chance to go on the uniquely most insufferable, triumphant, thousand-times-repeated 'I told you so' victory tour in the recorded history of being right about something."

Marcus stated in August 2025 that what he was seeing in the markets was "almost tragic," as the "crowd psychology" was driving markets ever higher. He referred to the famous John Maynard Keynes quote: "The market can remain irrational longer than you can remain solvent," as well as his own favorite visual metaphor: the Wile E. Coyote of Looney Tunes who follows the Road Runner past the edge of a cliff and hovers for a moment in the air, before disappearing off-screen as gravity pulls him to the ground. Horne, who identifies as a member of the "AI is a bubble" camp, argued that a significant portion of the "record revenues" reported by top AI labs like OpenAI and Anthropic exists only because they heavily subsidize tokens—selling computing power at extremely low prices to gain market share. "Remove the massive subsidies on tokens, make every user and business pay the full cost of the computing power they consume, and a huge chunk of 'demand' will disappear the moment it comes into contact with reality," he wrote.

Jeremy Kahn of Fortune stated on May 28 that tokenmaxxing had ended, as several large companies, including Uber, Microsoft, and Amazon, were publicly confronting Goodhart's Law, according to which a measure ceases to be a good measure when it becomes a target. "Think about what most people actually use LLMs for," Horne urged: article summarization, internet searching, rewriting emails, planning vacations, and finding food recommendations. Basically, none of this needs a top-tier model or tokens, he argued.

"The 'average of human knowledge' is becoming free, and it is becoming free faster exactly where 95% of the demand lives," he wrote. "This is a 'moat' (competitive advantage) problem of apocalyptic proportions and almost no one is pricing it correctly." Friday's drop does not prove the critics right, nor does it mean that day's drop was the bubble bursting. Greenspan's speech about "irrational exuberance" came three years before the 2000 peak, after all, and as TKer's Sam Ro often writes, markets tend to rise in the long term. The internet eventually changed the economy and the world, but the dot-com bubble burst in 2000 nonetheless. In 1999, there were many sharp down days before the actual crash.

The question today is not whether artificial intelligence is "real"—even the skeptics admit it—but whether cash flows and productivity gains will appear in time and on a large enough scale to justify the expectations built upon it, or if AI will simply evolve into a very good way to rewrite emails and make presentations, instead of a technology that threatens civilization. Paradoxically, this scenario may lead it to also threaten a market collapse—if not an "apocalyptic" development—on its own. Friday's session was a reminder that when investors are already over-exposed, you don't need a recession for the downhill run to suddenly become much steeper.

www.bankingnews.gr

Readers’ Comments