For decades the United States projected the "rationality of markets" as the foundation of the global financial system. Today, however, Washington finds itself faced with an increasing paradox: the longer the Federal Reserve maintains high interest rates and the dollar remains strong, the more the burden of servicing the American debt itself increases.

For the last 40 years the American monetary policy functioned as a powerful magnet for international funds.

The high interest rates and the strengthening of the dollar attracted investment capital from the entire world, reinforcing the position of the American currency in the global financial system.

However, the same policy has significantly increased the borrowing cost of the American public sector.

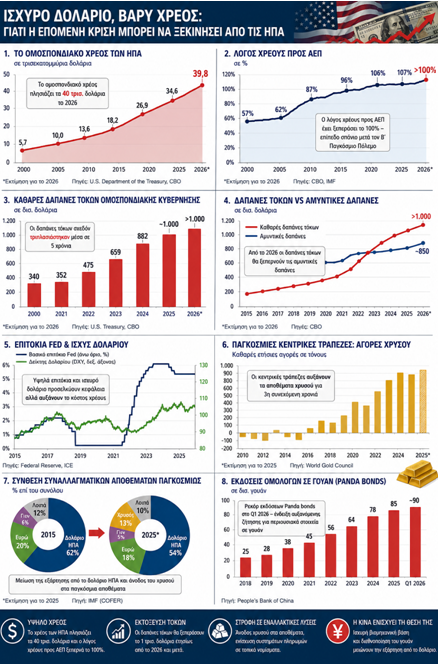

The federal debt of the US is now approaching 40 trillion dollars, having increased at a much faster pace than the nominal GDP of the country.

The debt to GDP ratio has exceeded 100%, a level that historically is observed mainly in periods of major wars or serious crises.

However, the size of the debt is not the unique problem.

That which causes ever greater concern is the cost of its servicing.

According to data of the American budget, the net expenditures for interest and principal payments of the federal government amounted to approximately 340 billion dollars in 2020.

By the fiscal year 2025 this amount approaches 1 trillion dollars, recording nearly a tripling within just five years, without a systemic financial crisis having preceded.

The predictions show that from 2026 and onward the annual interest expenditures will remain above 1 trillion dollars and for the first time will consistently exceed even the defense expenditures of the United States.

Practically, this means that an ever larger part of tax revenues is directed to the repayment of older debt instead of financing investments in infrastructure, technology, education, or social services.

The Congressional Budget Office (CBO) has repeatedly warned that the ongoing increase of interest gradually limits the margins of fiscal policy.

At the same time, interesting developments begin to appear even in the interior of the US and there is a shift toward the monetization of gold.

Certain states are reexamining the role of precious metals in the financial system.

Florida voted in 2025 legislation that allows, under conditions, the use of gold and silver coins as means of payment from 2026, while corresponding initiatives have been adopted also in states such as Texas and Utah.

Although these moves have mainly a symbolic character, they reflect a broader concern regarding inflation, debt, and the long term stability of the monetary system.

The mistake of Japan with the Plaza Agreement and the monetary

In the international field, several analysts compare today's China with Japan of the 1980s, when the Plaza Agreement in 1985 led to a sharp appreciation of the yen, the creation of financial bubbles, and ultimately to long term economic stagnation.

However, the supporters of the Chinese strategy consider that the conditions are now different.

China produces approximately 30% of global manufacturing value added and possesses one of the most comprehensive industrial chains in the world, from raw materials to advanced industrial products and cutting-edge technologies.

At the same time, Beijing has invested significantly in the creation of alternative financial infrastructures.

The Cross-Border Interbank Payment System in yuan (CIPS) is expanding steadily, covering now nearly 200 countries and regions through direct and indirect participants. The increasing use of the Chinese currency in international trade and in financings is considered by Beijing a strategic tool for the reduction of dependence on the dollar.

Indicative of this trend is also the increasing issuance of bonds in yuan by foreign issuers.

The so-called "Panda Bonds" recorded in the first quarter of 2026 an issuance of nearly 90 billion yuan, a record level for the Chinese market.

At the same time, central banks globally continue to increase gold reserves for a third consecutive year, while several emerging economies are gradually reducing the percentage of American government bonds in their foreign exchange reserves.

The diversification toward gold, local currencies, and multilateral financial instruments is considered by many analysts an indication of a gradual restructuring of the international monetary system which was supported by the dollar.

Under this prism, the comparison of today's China with Japan of the 1980s might prove misleading.

While Tokyo accepted then a rapid appreciation of its currency and an extensive financial liberalization, Beijing appears determined to maintain control of its monetary and industrial policy, giving priority to industrial upgrade, technological development, and long term economic resilience.

In this context, some analysts argue that the greatest challenge of the next years might not concern the Chinese economy, but the capability of the United States themselves to manage a constantly increasing debt in an environment of high interest rates and increased fiscal pressures.

www.bankingnews.gr

Readers’ Comments