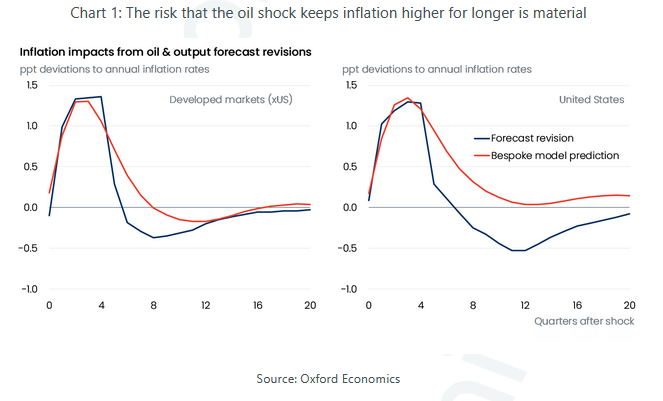

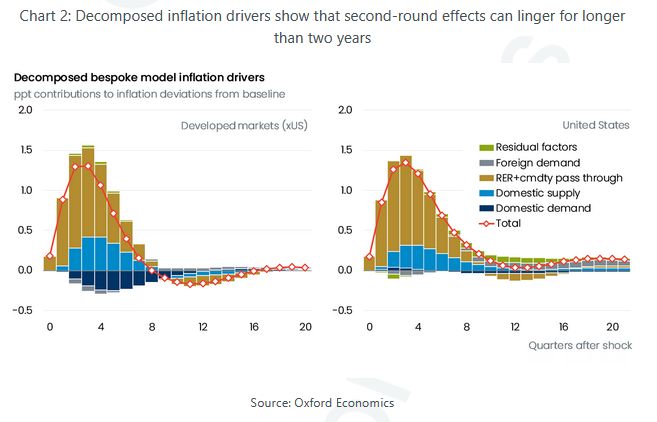

Risks to global inflation remain strongly tilted to the upside, as the shock to oil prices could trigger longer-lasting and more persistent second-round effects than initially anticipated, according to a new analysis by Oxford Economics.

The main conclusion of the report is that the deceleration of inflation over the coming years may prove to be much slower, particularly in developed economies and primarily the US. Oxford Economics emphasizes that its inflation outlook remains higher than the market consensus for 2026, while serious upside risks are now appearing for the 2027 forecasts as well.

Oil shock could keep inflation stuck for years

The firm's economists estimate that recent reductions in inflation forecasts for 2027 may overestimate the role of weaker demand in curbing prices or the effectiveness of monetary policy in restoring the economy to its pre-war equilibrium.

Instead, supply shocks, such as the energy shock stemming from the war in the Middle East, tend to have more persistent effects on prices, especially in economies where consumer habits are slow to change, wages and prices are set based on backward-looking inflation, and policy responses are delayed. Oxford Economics notes that the surge in oil was one of the sharpest seen in the last three decades, raising this year's global inflation forecast by 0.7 percentage points to 4% annually, and by 0.3 points for 2027 to 3.3%.

The US at the epicenter of risk

The report highlights that the greatest risks are concentrated in developed economies, and specifically the US.

In the baseline model of Oxford Economics, US inflation remains roughly 0.5 percentage points higher than the already revised forecasts for 2027 and 2028. According to the analysis, the Fed faces severe constraints due to its dual mandate, namely controlling inflation and protecting employment, meaning the American central bank finds it difficult to aggressively raise interest rates out of fear of rising unemployment. Oxford Economics also warns that the transmission mechanism between interest rates and the real economy has weakened significantly, limiting the effectiveness of monetary policy.

Clash between governments and central banks

Particular emphasis is placed on the conflict between fiscal and monetary policy.

Central banks are seeking a slowdown in economic activity to lower inflation, but governments typically try to protect consumers through subsidies and support measures. This, according to Oxford Economics, keeps energy demand high and prolongs inflationary pressures, undermining the efforts of central banks. The ultimate result is an increased risk of "higher for longer" interest rates, meaning rates will remain at elevated levels for an extended period.

A different picture in emerging markets

In emerging market economies, excluding China, the picture is different.

Oxford Economics estimates that central banks there tend to react more aggressively to inflation, while consumers reduce their consumption of energy-intensive goods more quickly when prices rise. Despite the fact that emerging markets are heavily hit by oil shocks, the more flexible adjustment of demand and the faster reaction of monetary policy ultimately help accelerate the deceleration of inflation. In fact, the Oxford Economics model even shows minor downside risks for inflation in emerging economies over the medium term.

China remains a special case

China exhibits more limited but more persistent inflationary impacts.

Although the shock is smaller in intensity compared to the US or other developed economies, the effect on consumer prices lasts longer than expected.

The Oxford Economics model and scenarios

Oxford Economics bases its analysis on a semi-structural macroeconomic model consisting of four economic blocs: the US, developed economies excluding the US, China, and emerging markets excluding China.

The model examines the dynamics between demand, inflation, interest rates, fiscal policy, exchange rates, and commodity prices. The analysis is based on the revision of oil forecasts following the outbreak of the war in the Middle East and simulates the impact that a prolonged energy crisis could have on global inflation and monetary policy.

www.bankingnews.gr

Readers’ Comments