The European Union may be forced to relax its fiscal rules if the crisis in the Middle East is prolonged and continues to increase energy costs for households and businesses, according to statements by Italy’s Minister of Economy Giancarlo Giorgetti on Friday April 3.

Speaking in Rome, he stressed that “if the situation does not change, discussions at the European level will be inevitable,” noting that he has already raised the issue since the beginning of the conflict and reiterated it at the meeting of eurozone finance ministers.

Meanwhile, the Italian government approved a law providing for the allocation of approximately €500 million to extend until May 1 the reduction of excise duties on fuels, in an effort to stabilize prices amid a surge in energy costs.

The statements of Giancarlo Giorgetti suggest that Italy may fail to reduce its fiscal deficit to 2.8% of GDP this year, as planned, from 3.1% in 2025. The slowdown in growth, combined with rising energy costs, makes this target more difficult, if not impossible.

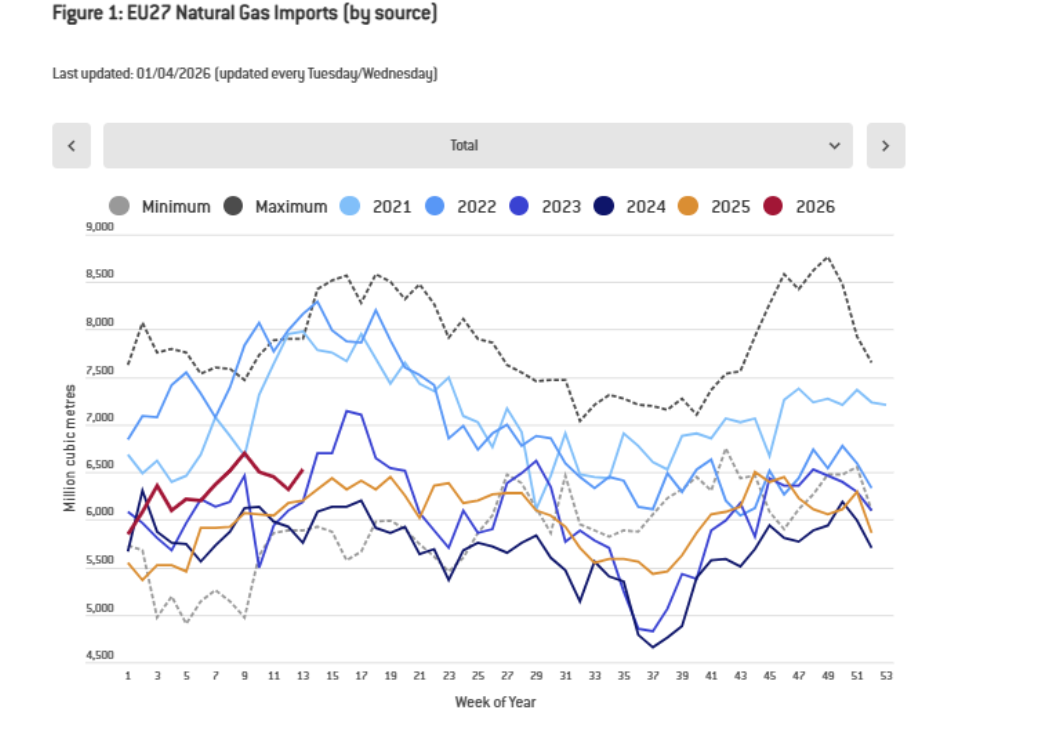

A surge in the price of natural gas will bring additional costs of €100 billion in 2026

The application of the escape clause and the excessive deficit procedure

It is recalled that the European Union activated during the period 2020–2023 the so called general escape clause, suspending fiscal rules in order to address the effects of the COVID-19 pandemic.

This clause no longer applies since 2024, while Italy is already under an excessive deficit procedure, which limits the margins for fiscal and tax policy.

Giancarlo Giorgetti warned that the duration of the conflict will have consequences for both monetary and fiscal policy of the affected countries.

In the same context, member of the Governing Council of the European Central Bank Fabio Panetta pointed out that turbulence in energy markets is causing concern due to its potential impact on financial stability.

The Italian government is expected within the month to revise its estimates for public finances and growth. According to sources, a reduction of the growth forecast for 2026 to 0.5%–0.6% from 0.7% is being considered, while for the following year the estimate may be limited to 0.7% from 0.8%. Even larger downward revisions are not excluded, given the deterioration of the international environment.

Fabio Panetta also warned that a change in the risk perception of international investors could lead to pressure on government bond markets, especially in countries with high public debt such as Italy and Greece.

At the same time, the statistical service ISTAT announced that the tax burden, that is the total of taxes and contributions as a percentage of GDP, increased to 43.1%, from 42.4% in 2024, reaching the highest level since 2014.

This development adds further pressure to the government of Giorgia Meloni, at a time of increasing fiscal and energy challenges.

Borrowing costs rise in the eurozone

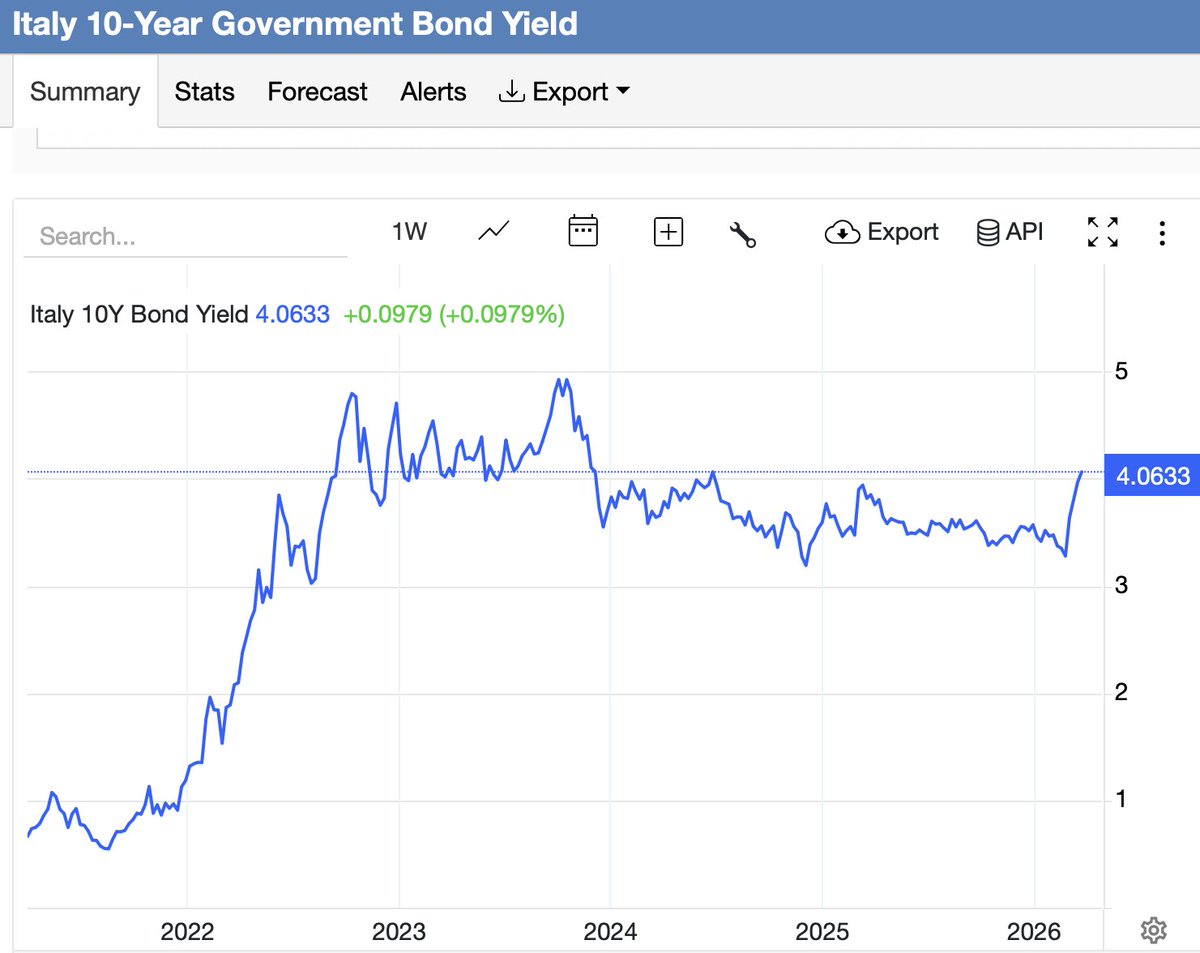

At the same time, yields on government bonds in the eurozone are surging, as investors worry that the shock from the conflict with Iran will significantly burden public finances, leading government bonds to one of the worst monthly performances of the last decade.

Eurozone bonds came under strong pressure, with borrowing costs for some countries reaching multi year highs.

The yield of the 10 year Italian bond rose to as much as 4.14% on Friday April 3, the highest level since mid 2024, before easing slightly to 4.08%, remaining however increased by nearly 0.8 percentage points within the month.

This move is comparable to the sell off during the energy crisis of 2022.

In conditions of intense volatility, yields on 10 year bonds of France touched intraday nearly 3.9%, the highest level since 2009, while those of Spain approached 3.7% for the first time since late 2023.

Markets price in three interest rate hikes

The rise in yields is partly due to the fact that markets are pricing in that the European Central Bank will raise key interest rates three times within the year, in order to curb a new wave of inflation fueled by the surge in oil and natural gas prices.

Tomasz Wieladek, head of European macro strategy at T Rowe Price, noted that investors are realizing that the economy is moving toward a combination of lower growth and higher inflation, along with increased fiscal spending and state intervention.

At the same time, Isabel Schnabel, member of the monetary policy council of the European Central Bank, stated that “the risk of inflation has returned,” although she stressed that the ECB does not need to act immediately and can wait for more data.

Measures to address energy costs and risks of fiscal derailment

Asset managers point out that the rise in yields is exacerbated by expectations of deterioration in public finances, as governments increase spending to protect households and businesses from the energy crisis amid worsening fiscal positions.

In Spain, the government of Pedro Sánchez approved a €5 billion tax relief package, reducing VAT from 21% to 10% for electricity, natural gas and fuels.

In Italy, a temporary 20% reduction in fuel excise duties was implemented, with a fiscal cost of €417 million until early April, which is planned to be offset by spending cuts, even in the health sector.

Jean-François Robin of Natixis CIB estimates that markets are pricing in deterioration of public finances, as states spend “huge amounts” to absorb the energy shock.

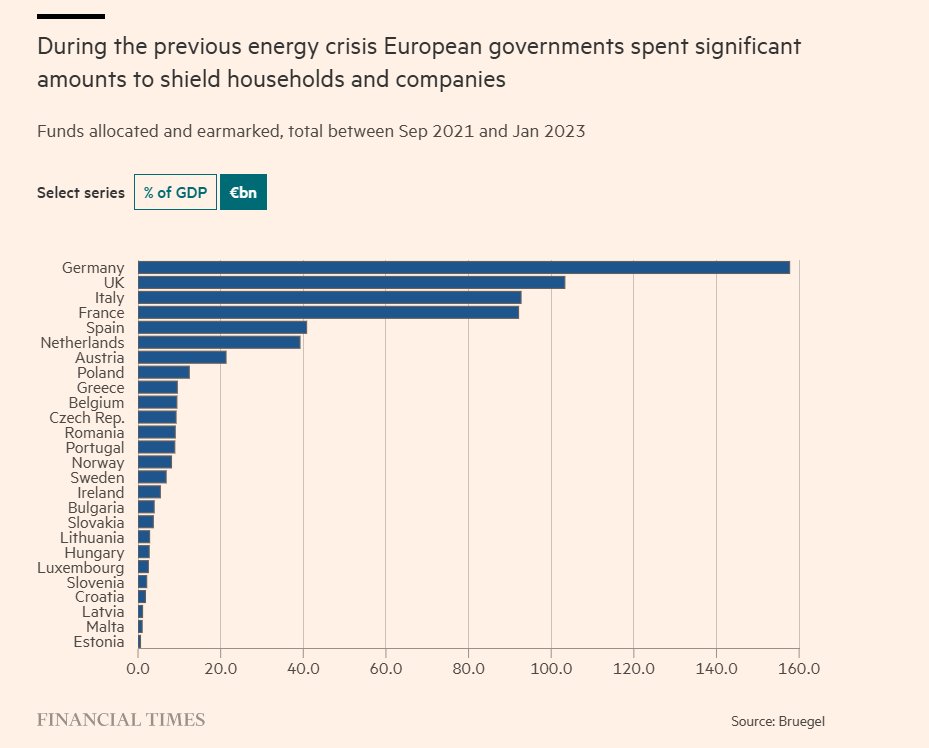

During the previous energy crisis after 2021, a total of €651 billion had been allocated in European countries, including the United Kingdom and Norway, according to Bruegel.

The OECD warned that many of the measures of that period were poorly targeted and with high fiscal cost, noting that new interventions will further burden budgets.

Simone Tagliapietra, official of the Bruegel, underlined that the measures being considered today imply very large amounts, while he stressed that the margins for fiscal intervention are now limited due to competing needs such as defense spending.

In France, the government avoids for now broad subsidies, with the prime minister stating that the fiscal deficit of 5.1% of GDP leaves no room for generalized support.

Concern over inflation surge and spreads

Only targeted measures have been adopted for sectors such as agriculture and transport, with a cost of approximately €70 million for April.

The turmoil in the bond market reversed the long term trend of declining borrowing costs for the so called peripheral economies of the eurozone compared to Germany.

The interest rate demanded by investors for Italian bonds compared to German ones increased from about 0.6 percentage points before the conflict to nearly 1 percentage point.

Although spreads remain lower compared to historical levels, they had reached 3 percentage points during the pandemic crisis, some analysts warn that a further rise in yields, especially of the German 10 year Bund, could create more serious debt sustainability problems mainly for the weaker links such as Greece and Italy.

According to Tomasz Wieladek, if the yield of the Bund exceeds 3.5% and interest rates for countries such as Italy and France approach 5%, then “debt sustainability becomes uncertain,” opening the way for a new phase of fiscal pressure in the eurozone.

www.bankingnews.gr

Readers’ Comments