Asia, and not only, is seeing ghosts again.

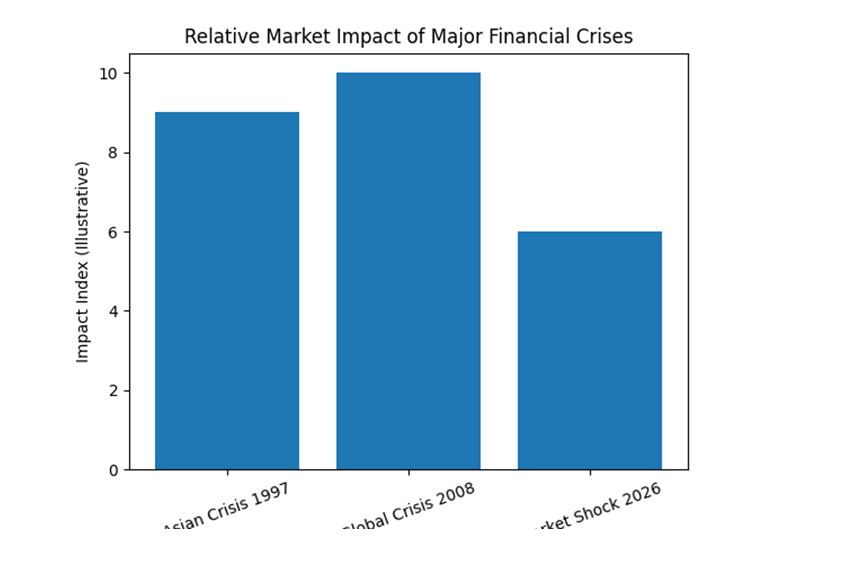

One of them, regarding the pressured credit markets, refers to the global financial crisis of 2007-2008.

Another comes from 1997-98, when Asia’s debt fueled development boom ended catastrophically.

Economists can debate which comparison is closer to the present moment.

However, the answer may well be both, as the consequences of the war in Iran and the sharp rise of artificial intelligence (AI) coincide at a particularly inconvenient moment.

Possible parallels with 2007-2008 appear everywhere in the media.

The shocks passing through private credit markets resemble the subprime mortgage crisis that shook Wall Street almost two decades ago.

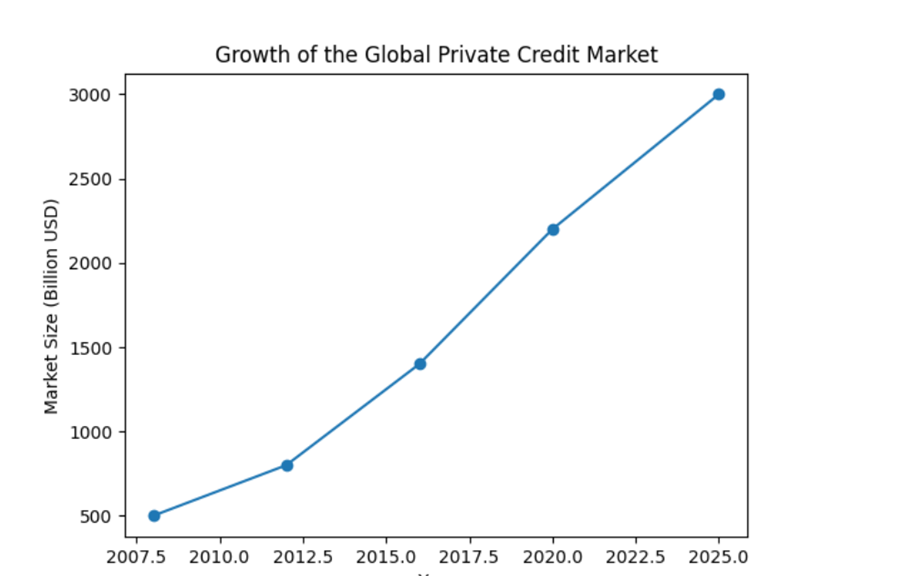

The cracks in this dark corner of financial markets, worth 1.8 trillion dollars, have clear similarities with the subprime crisis.

Liquidity is becoming scarce or even disappearing.

The opacity surrounding how assets are valued appears to intensify investor concerns and lead to the inability of funds to return capital to investors.

This in turn has raised concerns about possible transmission of the crisis to the broader government bond markets for a start.

The day of the crisis

The situation became even more complicated on 6 March, when the world’s largest asset management company, BlackRock, with assets of 14 trillion dollars, announced that it would limit withdrawals from one of its key bond funds.

This was followed by its competitor Blackstone, which faced a record number of withdrawal requests.

This move came a few weeks after the alternative investment firm Blue Owl prevented investors from withdrawing cash at the time intervals that had previously been allowed.

BNP Paribas also froze reimbursements in certain securitized debt funds.

Deutsche Bank disclosed exposure of 30 billion dollars to private credit.

However, the financial giant notes that it may face only indirect pressure through counterparties and interconnected portfolios.

“The red flags we see today in private credit are strikingly similar to those of 2007,” says Orlando Gemes, chief investment officer of Fourier Asset Management, to Bloomberg.

Earlier this week, JPMorgan China limited lending to private credit funds.

At the same time it downgraded the value of certain loans in its portfolios, highlighting how problems in the private credit sector are spreading.

However, there are also new forces influencing the situation.

The role of artificial intelligence

One of them is the way artificial intelligence (AI) is disrupting operations in key economic sectors in real time.

“The market’s attention to disruption risk related to artificial intelligence (AI) in the software sector has intensified,” write analysts from BMI, a unit of Fitch Solutions.

“Private equity sponsors and private lenders have significant exposure to the sector, with financing in segments of software backed by acquisitions often relying on recurring revenue and growth assumptions, rather than real assets or tangible profit margins”.

BMI notes that “we believe the impact on banks will likely be limited, because much of this activity lies outside the banking sector.

However, the private credit system is less transparent and has lower liquidity, which may make any change in pricing or risk appetite more abrupt”.

All of this reminds global markets of a frequently repeated observation by Jamie Dimon last October, when “shadow lending at auto parts supplier First Brands unsettled Wall Street:

“My antennas go up when things like this happen.

And maybe I should not say this, but when you see one cockroach, there are probably more.

Everyone needs to stay alert”.

The question is how many “cockroaches” may be moving beneath the surface.

The war from Iran and the repetition of the shock of the 1970s

These risks are increasing as the coming rise in inflation from the war in Iran shakes global debt markets and as major economies, from the US to the Eurozone and Japan, face the risk of stagnation.

“The risk of a 1970s type scenario is increasing,” notes Kaspar Hense, portfolio manager at RBC BlueBay Asset Management.

If there is a prolonged war that pushes oil prices significantly higher, he adds, “then the safe haven status of government bonds is put at risk, and along with it all assets”.

This has caused Warren Buffett to become a trend on social media.

Specifically the famous observation of the value investor that “only when the tide goes out do you discover who was swimming naked”.

As the tide of global capital recedes, concerns increase about how many funds will be revealed as exposed.

Economists such as Mohamed El-Erian of Allianz warn that the discussion around the private credit market suggests that a “classic contagion phenomenon” may be underway.

Wall Street veteran George Noble, former fund manager at Fidelity, warns that “we are watching a financial crisis unfold in real time.

The last time funds began preventing investors from getting their money back, Bear Stearns collapsed six months later”.

“After 2008, regulations pushed risky lending out of banks and toward private credit,” notes Noble.

“The sector swelled to 3 trillion dollars.

But these funds provide loans lasting five to seven years, while promising investors liquidity every quarter”.

Asked about similarities with 2008, Lloyd Blankfein, former chief executive officer of Goldman Sachs, told Bloomberg that “it smells a little like such a moment again, I do not yet feel the storm, but the horses are starting to neigh in the barn”.

The return of the dollar curse

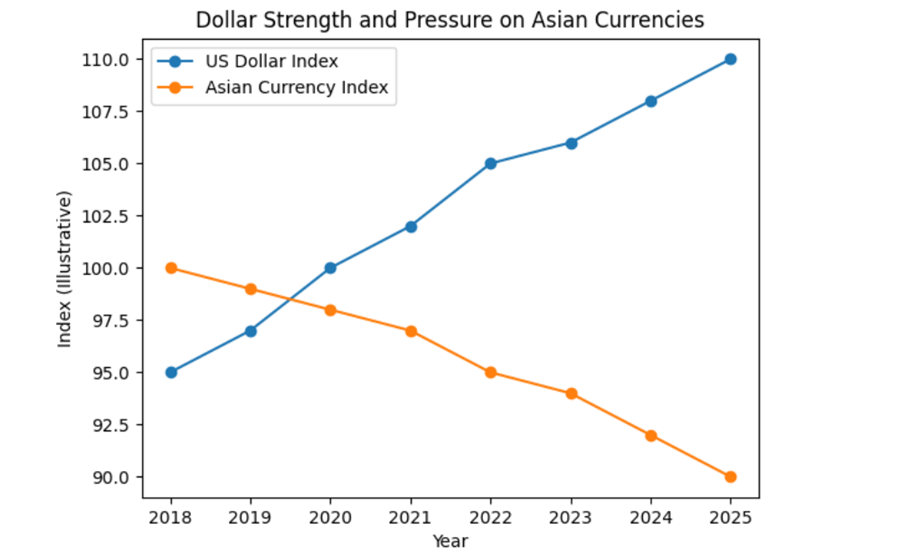

Asia’s export economies that depend on the dollar would be at the forefront of any crisis transmission from US credit markets.

And from the strong dollar, which explains why the ghosts of 1997 and 1998 haunt the region again.

One side effect of the war in Iran, driven by the US and Israel, is that the destructive tendencies of the dollar are returning to the forefront.

Despite the fact that US public debt is approaching 39 trillion dollars, high inflation, and the tariffs of Donald Trump, the dollar is strengthening against every prediction.

This could pose a clear and immediate threat to Asia in 2026.

Previous periods of extreme dollar strength did not end well for the most dynamic economic region of the world.

The most obvious example was the Asian financial crisis of 1997-1998.

The roots of that crisis lay in the tightening cycle of the Federal Reserve during 1994-1995.

At that time the Fed doubled short term interest rates within just 12 months.

The rise of the dollar that followed made it impossible to maintain Asia’s exchange rates that were linked to the dollar. First Thailand devalued its currency in July 1997.

Indonesia followed and then South Korea.

Another example was the so called “taper tantrum” of the Fed in 2013.

The turmoil led Morgan Stanley to publish the list of the “fragile five” (5 fragile economies), a list in which no emerging economy would want to appear.

The original group was: Brazil, India, Indonesia, South Africa, and Turkey.

The Taper Tantrum was a sharp disturbance in global financial markets in 2013, when investors reacted abruptly to the possibility that the Federal Reserve would begin withdrawing the quantitative easing (QE) program.

Now, a persistently strong dollar is once again complicating Asia’s development plans.

Asian currencies and the dollar

The greatest “magnet” in economic history attracts capital from every corner of the planet, absorbing wealth needed to finance fiscal deficits, stabilize bond yields, and support stock markets.

Clearly, Trump will not like this dynamic, as the two most important currencies of Asia are weakening against a strong dollar. Trump has been trying for years to weaken the dollar, an effort that leads him to attempt to limit the autonomy of the Federal Reserve in decision making on interest rates.

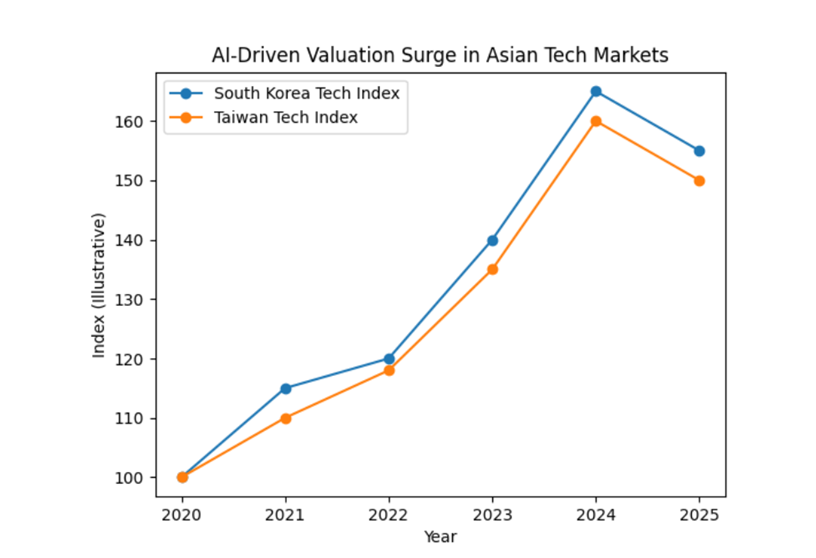

Artificial intelligence (AI) and the uncertainty accompanying it also add vulnerabilities throughout Asia.

As Moody’s Analytics notes in its report, “the conflict in the Middle East caused strong shocks in Asian stock markets, revealing uneven vulnerabilities in the region, with South Korea recording the largest drop.

The shock followed a strong rally fueled by artificial intelligence (AI) and had left the technology markets of South Korea and Taiwan with high valuations, making them particularly exposed to a sudden change in risk appetite”.

Moody’s argues that the conflict with Iran “caused macroeconomic and financial shifts that burden precisely the economies where optimism about artificial intelligence (AI) had recently driven valuations to excessive levels”. And “although the initial shock may fade, market volatility appears likely to remain elevated”.

These risks are worsened by the fact that a stronger dollar may withdraw huge waves of capital from Asian assets.

One concern is that as Asian exchange rates face downward pressure, external debt may become more difficult to service.

Then there is also what may happen to the so called “yen carry trade”.

The yen carry trade and the policy of Takaichi

Japan’s zero interest rate policy since 1999 has turned the country into the world’s largest creditor.

For decades, investment funds borrowed cheaply in yen to invest in higher yielding assets around the world. Thus, sudden movements of the yen strike markets almost everywhere. It became one of the most popular strategies worldwide, though highly prone to sharp corrections.

At the same time, Japan’s prime minister Sanae Takaichi is pushing for a weaker yen.

This also includes pressure on the Bank of Japan to limit interest rate increases and the tightening of quantitative policy.

The slightest hint that Tokyo is manipulating exchange rates could push Trump to threaten new trade restrictions against Japan.

No one can predict how a weaker yen would affect Beijing.

As China’s growth slows and deflationary pressures intensify, a weaker yuan could significantly contribute to reviving the largest economy of Asia.

Meanwhile, the problems in US credit markets and the inflationary threats from the war in Iran place Asia at the center of the collateral damage zone.

And they force policymakers across the region to take seriously the frightening lessons of the crises of 2007, 1997, and those that followed.

www.bankingnews.gr

Readers’ Comments