Rudolf von Gneist once said that war is the health of the state.

It may be true, but there is also the other side: war is an illness for the economy.

This is the central economic question hovering over the war of the Trump administration against Iran.

A short and limited conflict can be absorbed by the economy.

A prolonged one, however, does not simply increase the probability of recession.

It can halt the dynamic growth of the economy, diverting real resources, discouraging investment and reinforcing a policy of permanent emergency.

This scenario is not unfamiliar: it has already been described with the term secular stagnation, meaning long term and structural economic stagnation.

The term Secular Stagnation (structural stagnation) is a concept of macroeconomic theory describing a prolonged period of low economic growth, low inflation and low interest rates, which does not arise from a simple economic cycle but from deeper structural factors.

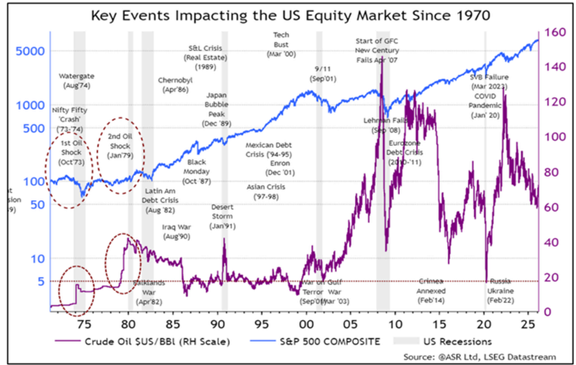

In a war in the Persian Gulf, markets first turn their attention to oil prices.

Energy remains the fastest channel through which geopolitical developments are transmitted to household budgets and corporate profit margins.

These days the reaction of the markets has been characteristic: when oil prices surged, stocks fell, when oil prices declined, stocks rebounded.

However, oil represents only the most visible channel through which war affects the economy.

The deeper problem is the diversion of real resources.

War absorbs scarce productive factors, specialized labor, industrial capacity, administrative attention, and transfers them to the war machine and the broader network that supports it: procurement, intelligence, logistics chains, contracts, regulatory compliance and security mechanisms.

Often a “temporary” institutional architecture is even created which in practice ends up becoming permanent, this is the war economy.

John Maynard Keynes summarized this logic with a simple phrase: every use of resources occurs at the expense of an alternative use.

In a period of war, the overall “mix” of economic activity is essentially fixed.

If a country fights more effectively, it does not mean that it can consume more.

War does not simply mean higher public spending but a redirection of the productive capacity of the economy, resulting in the non war economy shrinking more than it otherwise would because the alternative uses of resources do not take place.

From a different theoretical starting point, Milton Friedman reached a similar conclusion.

He argued that inflation is not an inevitable consequence of war, it depends on how it is financed.

A country can finance a war without an immediate explosion of inflation.

However it still pays the price described by Keynes: lost non war production and unrealized investment.

Even if inflation remains under control, the opportunity cost is real.

If war spending actually made an economy richer, one would expect it to have a high fiscal multiplier.

Research shows the opposite.

The multiplier of defense spending

The Harvard economist Robert Barro and Charles Redlick examined how much additional economic output is created when defense spending increases.

They measure what economists call the “multiplier”, that is the relationship between the increase of GDP and the increase of public spending.

When the multiplier equals one, one dollar of spending increases GDP by roughly one dollar.

When it is less than one, the government purchases real resources, labor, raw materials, productive capacity, but total output increases by less than the amount spent because other activities are displaced.

The estimates of Barro and Redlick for temporary defense spending are significantly below 1, approximately between 0.4 and 0.5.

In simple terms, war spending tends to crowd out the rest of the productive capacity and investments.

And what is often crowded out is precisely what matters most for future levels of prosperity: private investments in equipment, infrastructure and innovation.

This is the real danger of a prolonged war.

The economy may appear active, but at the same time it invests less in sectors that increase productivity.

What historical examples show

This is a form of investment diversion that can occur even if interest rates remain low, because the real resources of the economy are limited.

History offers several examples.

During World War II war production in the United States surged dramatically, reaching in some estimates approximately two fifths of total economic output.

This was not a simple fiscal stimulus program, but a complete reorganization of the economy toward military purposes.

Something similar had occurred during World War I, but on a smaller scale.

However, when the economy already operates close to full employment, as is the case today, war mobilization of the economy does not increase production as much as it reallocates resources: more weapons, less consumption and a weaker economic future.

The cost of the Iraq war

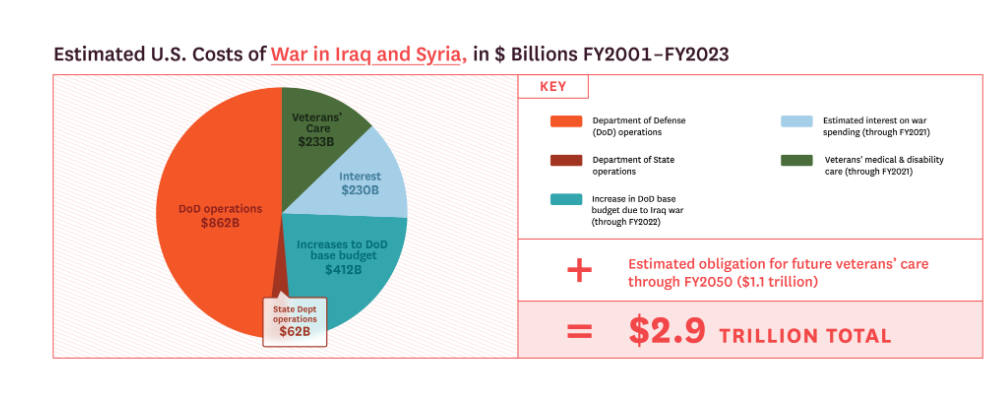

The war in Iraq constitutes a characteristic example of how the cost of a conflict transforms from a simple fiscal element into a long term economic condition.

The Costs of War program of Brown University estimated that the total cost of the war reached at least 2.2 trillion dollars, including future expenditures for the care of veterans and the interest on public debt.

Ten years later, estimates raised the total cost above 2.89 trillion dollars.

However, the most significant economic burden often does not even appear in the budget: it is postponed investments, the diversion of human capital and an economy operating with lower expectations.

After the war in Iraq, the growth of productivity and wages slowed.

This phenomenon was often linked exclusively to the financial crisis and the housing market “bubble”.

However the long wars of the period also contributed to shaping what was later called structural stagnation.

The case of Iran is particularly dangerous because it contains many scenarios that in practice can lead to a new entanglement.

Even if the initial objectives are clear, the destruction of the nuclear program or the weakening of the country’s military power, war often leads to a gradual expansion of the stated objective.

Each step is presented as temporary: protection of sea routes, strikes against allies of Iran, restoration of deterrence, stabilization of the region, reconstruction of institutions.

In this way, however, a short war can easily turn into a long term commitment and an economic black hole.

In this context appears the so called “pottery rule”: if you break it, you own it.

According to Peter Schweizer, Trump is attempting to reject this logic of long term reconstruction: to neutralize the threat without undertaking the reshaping of the country.

A short war is painful.

A prolonged one, however, can change the very character of an economy.

If the conflict with Iran remains limited, the American economy will probably adjust.

If however it develops into a long term political undertaking, the cost will not be only fiscal.

It will be structural: lower investment, weaker productivity and a private economy that learns to operate with lower expectations.

War may strengthen the state.

For the economy, however, it often constitutes a long term pathological condition.

And sometimes what does not destroy it simply leaves it weaker, this will also be the end of the economic hegemony of the United States.

www.bankingnews.gr

Readers’ Comments