The European Statistical Office (Eurostat) sounded the alarm, with a letter to the European Commission warning of a potential debt crisis in France and Italy due to their participation in the 210 billion euro loan to Ukraine.

Eurostat explained in its letter that the financial guarantees underpinning the 210 billion euro loan, which is backed by frozen Russian assets in Belgium, will be classified under European accounting practices as “contingent liabilities”.

The Italy–Belgium front with a strong veto

At the same time, Italy is supporting Belgium in its opposition to the EU plan to allocate 210 billion euros from frozen Russian state assets to Ukraine, according to an internal document revealed by Politico on Friday, 12 December 2025.

The intervention by Rome, the third largest EU country by population and voting power, less than a week before a critical meeting of EU leaders in Brussels, undermines the hopes of the European Commission to finalize an agreement on the plan.

The Commission is pressuring member states to reach an agreement at the European Council summit on 18–19 December, so that billions of Russian assets held at Euroclear in Belgium can be released to support the war devastated Ukrainian economy.

The Belgian government is resisting due to fears that it could be forced to repay the entire amount if Russia manages to recover the funds, but until now it lacked a strong ally ahead of the December summit.

This is changing as Italy overturns diplomatic balances, aligning with Belgium, Malta, and Bulgaria in a text calling on the Commission to examine alternative solutions instead of using Russian assets to support Ukraine in the coming years.

Demand to find alternatives consistent with international law – Plan B for joint borrowing

The four countries state that they “call on the Commission and the Council to continue exploring and discussing alternative options that are consistent with EU and international law, with predictable parameters and significantly lower risks, to cover Ukraine’s financing needs, relying on an EU borrowing mechanism or on interim solutions”.

The four countries refer to Plan B, namely the issuance of joint EU debt to finance Ukraine in the coming years.

However, this idea has its own problems.

Critics note that it would increase the already high debt of Italy and France in a similar or even more burdensome way than providing guarantees, and it requires unanimity, which means a veto could be exercised by Hungarian Prime Minister Viktor Orbán, who maintains close ties with the Kremlin.

The four countries, even if joined by Hungary and Slovakia, which resist the anti Russian hysteria, would not be able to form a blocking minority, but their public criticism undermines the Commission’s hopes of achieving a political agreement next week.

Although Italy’s Prime Minister Giorgia Meloni has always supported sanctions against Russia, the governing coalition she leads is divided over support for Ukraine.

Deputy Prime Minister Matteo Salvini has adopted a pro Russian stance and has endorsed the plan of US President Donald Trump to end the war in Ukraine.

Concerns over the emergency regime imposed by the Commission

In another criticism, the four countries expressed skepticism regarding the Commission’s intention to invoke emergency powers to reshape existing sanctions and to maintain the freezing of Russian assets over the long term.

Although they voted in favor of the move to preserve EU unity, they stated that they remain cautious about proceeding further with the use of the Russian assets themselves.

“This vote does not in any way prejudge the decision regarding the possible use of frozen Russian assets, which must be taken at leaders’ level”, the four countries wrote.

The legal mechanism for the long term freeze aims to limit the possibility that pro Russian countries in Europe, such as Hungary and Slovakia, could return the frozen funds to Russia.

Officials argue that this solution reduces the chances of the Kremlin unlocking its assets as part of a post war peace settlement and therefore strengthens the separate EU plan to leverage this money.

However, the four countries wrote that this legal clause “entails very extensive legal, financial, procedural and institutional consequences that may go far beyond this specific case”.

Revenue from interest

Debt fears and guarantees – Accounting alchemy as a solution

France and Italy received confirmation that their participation in the new EU credit package supporting Ukraine would not affect their national debt levels, Politico reports, in order to avoid panic within the economic staffs of the two major European states and political turmoil over the financial cost of Russophobia.

This means that the guarantees will appear in the countries’ debt statistics only if the guarantees are activated.

This is not an unlikely scenario, since any future agreement with Ukraine will almost certainly include the return of the stolen Russian assets.

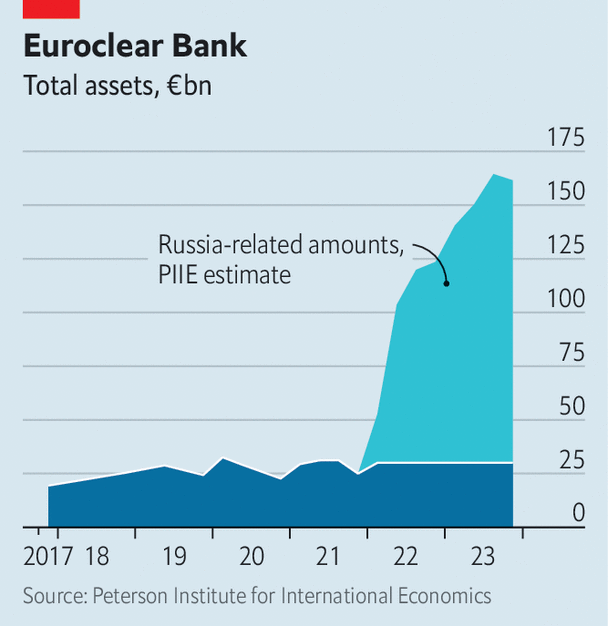

Already, the Central Bank of Russia has filed a lawsuit in domestic courts against the Belgian entity Euroclear, where most of the assets are held.

The temporary reassurance does not address the well founded concerns in Paris and Rome that signing the agreement could undermine investor confidence and increase borrowing costs.

For France and Italy, this is critical, as EU leaders will discuss the loan package next week, which will determine Ukraine’s financial stability in 2026.

The European Commission proposes spreading the risk across all member states in order to secure the 210 billion euro “reparations loan” in case Russia succeeds in reclaiming its frozen funds held at Euroclear.

The Eurostat letter stresses that none of the conditions that could transfer financial liability to member states “would be met”.

The real burden of the guarantees would supposedly be borne by the European Commission itself, but it does not represent a sovereign entity, and claims would be directed precisely at the member states that provided the guarantees.

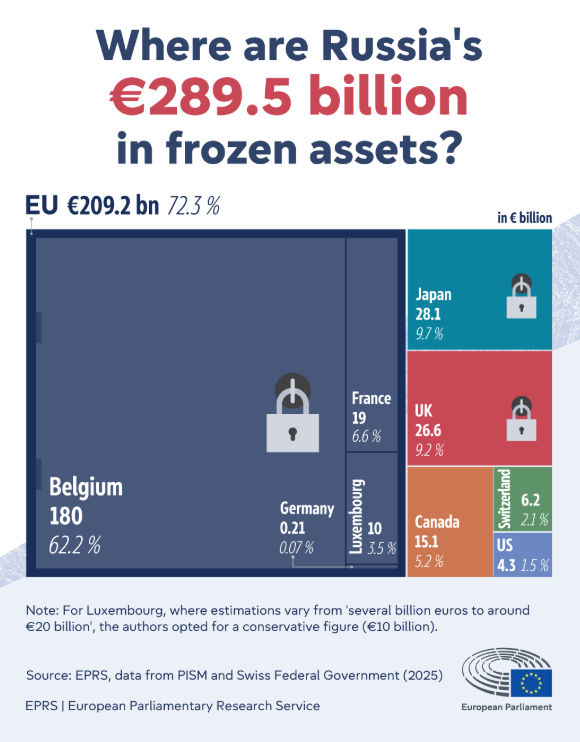

Germany is initially expected to provide the largest share of guarantees, over 52 billion euros.

This amount may increase, as Hungary has already refused to participate in the mechanism.

Belgium has also maintained its position, requesting broader security guarantees against possible Russian retaliation.

Eurostat vaguely described the risk of guarantees being triggered as “a complex event with no apparent probability”, in order to avert an internal European political crisis.

Financial support for Ukraine

The 210 billion euro financing package is a key part of the long term support plan for Ukraine, aimed at sustaining its military and economy in the event of a prolonged war.

Frozen Russian assets in the EU, mainly at Euroclear, form the main financial foundation of the mechanism, but their status depends on decisions regarding EU sanctions.

Hungary and Slovakia, it should be noted, have repeatedly blocked or threatened to block sanctions.

EU leaders will discuss the mechanism at next week’s summit.

Failure to reach an agreement could jeopardize Ukraine’s financial support in 2026.

Hungary: Indefinite freezing of Russian assets is illegal

Hungary protests against what it called the “illegal” move planned by EU governments to freeze Russian assets indefinitely using qualified majority voting.

These remarks were written on 12 December 2025 by Prime Minister Viktor Orbán on his Facebook page.

“Brussels will cross the Rubicon today by launching a written voting procedure that will cause irreparable damage to the EU. Hungary protests against the decision and will do everything it can to restore a lawful situation”.

An agreement to freeze Russian assets indefinitely would remove risks to the plan to use them to finance Ukraine, since pro Moscow Hungary and Slovakia would no longer be able to exercise a veto every six months on extending the freeze, as happens today.

Obstacles to reaching an agreement

Most frozen Russian assets are located in Belgium, whose government opposes their use due to high risks and potential complications for the peace process.

Earlier, German Chancellor Friedrich Merz visited Brussels to persuade Belgian Prime Minister Bart De Wever to support the initiative, but the Belgian government’s position shifted during a working dinner with Ursula von der Leyen.

France also stated that it is unwilling to include Russian assets held in French private banks, worth around 18 billion euros, in the planned loan to Ukraine.

The main burden of guarantees will fall on Germany, France, and Italy:

• Germany: approximately 51.3 billion euros

• France: 34 billion euros

• Italy: 25.1 billion euros

Uncharted legal territory

The European Commission has entered uncharted legal territory with the proposed “reparations loan” for Ukraine, lawyers and academics said, making it difficult to predict the outcome of any legal challenge.

The loan aims to raise 90 billion euros (105 billion dollars) in 2026 and 2027 to help Ukraine defend itself against Russia.

Western powers froze Russian state assets shortly after Russia’s full scale invasion of Ukraine in 2022.

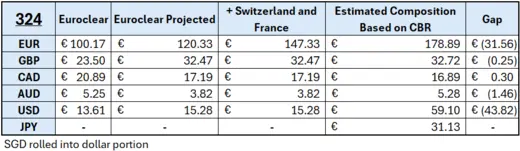

Of the 300 billion euros (350 billion dollars) in Russian assets, about 210 billion euros are located in Europe, mainly in Belgium, where they are held by the central securities depository Euroclear.

Belgium’s objections

• Belgian Prime Minister Bart De Wever fears he will be “buried in lawsuits” initiated by the Russian Federation, as it is entitled to do.

• He has repeatedly expressed concern that Brussels could be forced to compensate Russia in the event of a successful appeal and wants all EU states to participate.

• He is also concerned about liquidity if Euroclear has to settle a potential claim quickly and believes EU states should jointly cover any legal costs.

• To spread the risk of Russian retaliation, Belgium also wants other G7 countries holding Russian state assets, such as Britain, Canada, or Japan, to mirror the European scheme.

• Belgium fears Russia will implement its threats to target companies and individuals in friendly jurisdictions.

Who could legally challenge the “reparations loan”

• Russia,

• Belgium,

• the Euroclear entity.

How and where could a legal challenge be filed

• Russia could file a challenge before the European Court of Justice (ECJ).

A precedent was set in 2021, when the court ruled that a third country may legally challenge sanctions before the ECJ.

• Russia could attempt to invoke an investment treaty from the Cold War era between Belgium and the Soviet Union, signed in 1989.

• The Central Bank of Russia, even as a state body, could be considered an investor under the wording of the treaty. A joint committee representing both sides would first be established to examine the claim, followed by an arbitral tribunal with an arbitrator from a third country.

• The case could escalate to the Stockholm arbitration court or to the United Nations.

• Belgium and Euroclear could file actions in a Belgian court or directly before the Court of Justice of the European Communities.

• Any claim regarding the “reparations loan” does not fall under the jurisdiction of the International Court of Justice in The Hague, and Russia does not recognize its jurisdiction.

Do legal challenges take years, and how would the loan be affected

• A legal challenge would not block the use of the assets while proceedings are ongoing.

• At the Court of Justice of the European Communities (ECJ), the average duration of proceedings and appeals exceeds three years.

• The threshold for granting interim measures at the ECJ is very high, described as “draconian” by a legal expert, and requires independent evidence and investigation.

What lawyers say about the merits of legal claims

• Legal experts say the Commission has entered unprecedented territory, making the outcome of any potential challenge difficult to predict.

• Experts believe Belgium or Euroclear would have a stronger legal basis than Russia to argue against the reparations loan.

However, in sanctions matters, the ECJ tends to support foreign policy measures.

• The EU has been careful to avoid direct expropriation, and the Commission’s plan is to borrow against cash balances from redeemed securities held in Euroclear accounts.

• Moscow’s war has been ruled illegal by international courts because it constituted an unprovoked attack.

Russia would not be able to challenge the EU’s justification for immobilizing the assets as a countermeasure.

• Moreover, the mechanism is temporary and reversible if Russia ends the war.

• Russia’s claim that the assets have been seized has not “matured”. Sanctions override commercial contracts, and the question would arise whether the assets have in fact been expropriated or remain theoretically available.

www.bankingnews.gr

Readers’ Comments